MARKET UPDATE FOR THE WEEK 20TH APRIL

Global Macro Highlights

Global Growth Slows as Energy Shock Fuels Inflation Risks

The International Monetary Fund revised 2026 global growth down to 3.10% (vs 3.30%), driven by the Middle East conflict, with disruptions around the Strait of Hormuz impacting global energy supply.

Energy shocks pushed Brent crude to USD118.35/bbl (+34.58%), which is increasing inflation, reducing real incomes, raising business costs, and slowing household demand, investment, and overall global activity.

Weaker growth outlook points to softer trade and demand, with equities likely to rotate toward defensive sectors, while fixed income remains volatile as inflation and growth risks keep rate expectations uncertain and support safe-haven demand

China’s Growth Strengthens on Exports and Policy Support

China’s economy grew by +5.00% YoY in Q1:2026 (vs 4.50% in Q4:2025), driven by strong performance in services (+5.20%) supported by Al and digital activity, and industry (+6.10%) lifted by policy-backed equipment and high-tech manufacturing.

Growth was supported by fixed asset investment (+4.80%) in infrastructure and manufacturing, and strong exports (+11.90%) driven by EVs and green tech, as well as demand from ASEAN, the EU, and the UK, while real estate remained weak (-11.20%) and household consumption stayed subdued.

Overall, growth remains reliant on government stimulus and external demand, with domestic demand still fragile, and outlook is slightly softer as geopolitical risks and inflation could weigh on demand, although continued policy support should provide some cushion.

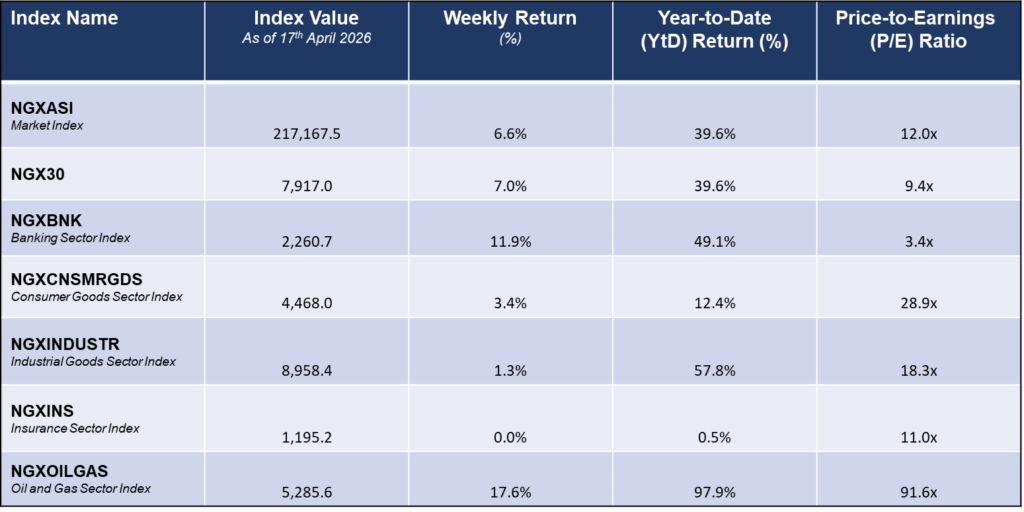

Global Equities Market – Sectorial Performance

Weekly Performance of Sectorial Indices

Domestic Events

Inflation Ticks Up, Clouding Rate Cut Outlook

According to the National Bureau of Statistics, headline inflation rose to 15.38% YoY in March 2026 (vs 15.06% in February), the first increase in 11 months, driven by persistent food and core price pressures.

Food inflation climbed to 14.31% YoY, while core inflation rose to 16.21% YoY, with transport, housing, and services costs increasing due to higher fuel prices and logistics constraints, even as MOM food inflation eased slightly to 4.17%.

The uptick complicates the upcoming MPC decision, as inflation remains above expectations and keeps a rate cut unlikely, with a hold more probable to keep borrowing costs elevated despite some moderation in monthly momentum.

Tariff Cuts Target Costs, but Inflation Relief May Lag

The Federal Government introduced tariff cuts across key imports with a 90-day transition from April 1, aimed at easing inflation and lowering transport and production costs, following President Tinubu’s directive amid rising fuel prices linked to the Middle East crisis.

Major reductions include vehicle duties cut to 40.00% (from 70.00%), full exemption on electric vehicles and mass transit buses, elimination of machinery import duties (from 5.00% ), and lower tariffs on food staples (rice, sugar, palm oil) and industrial inputs like steel and cement materials to reduce logistics, food, and construction costs.

Near-term inflation impact is expected to be limited due to weak pass-through from importers, meaning consumers may only see partial relief, while the most meaningful benefit is lower capital costs for manufacturers, supporting longer-term capacity expansion rather than immediate disinflation.

CBN Introduces NOFR to Strengthen Money Market Transparency

The CBN, in collaboration with FMDQ, has introduced the Nigerian Overnight Financing Rate (NOFR) as a new official benchmark rate to improve transparency, strengthen monetary policy transmission, and deepen the money market by providing a clearer reference for short-term funding costs. It is Nigeria’s equivalent of global risk-free benchmarks like SOFR (US), SONIA (UK), and TONA (Japan).

NOFR reflects the true cost of secured overnight borrowing in the interbank market, based on actual repo transactions backed by government securities (minimum NGN5bn), making it transaction-based rather than estimate-based. It is designed to reduce manipulation risk, improve pricing accuracy for instruments like T-bills and repos, and support fairer financial contract pricing.

It is now active with the CBN as benchmark administrator and is published daily at 10:00am, positioning it as the official overnight risk-free reference rate in Nigeria, alongside existing rates like OBB (secured interbank rate) and OVN (unsecured lending rate), while improving market consistency and aligning Nigeria with global best practice

Fixed-Income Market

In the primary fixed income market, the Central Bank of Nigeria (CBN) conducted OMO auction on Tuesday, offering a total of NGN600.0bn across the 7-day, 63-day, and 140-day tenors. Investor demand strengthened significantly, with total subscriptions rising by 99.0% to NGN2.6trn, translating to a subscription-to-offer ratio of 4.2x. The CBN ultimately allotted NGN2.2trn, resulting in a bid-to-cover ratio of 3.6x. Stop rates settling at 21.9% (7-day) and 19.9% for both the 63-day and 140-day papers.

The secondary T-bills market extended its bullish run, with average yield easing by 2bps to 17.4% from 17.5% the previous week, supported by persistent buying interest across the curve and the ample liquidity and reinvestment flows from maturing instruments. The most pronounced yield compression was observed on the MAR-27 (-27bps), SEPT-26 (-26bps), APR-27 (-26bps), and JUN-26 (-12bps) maturities. In contrast, selective profit-taking drove yield increases on the MAR-26 (+54bps) and FEB-27 (+14bps papers.

The secondary bond market also rebounded, reversing its earlier bearish trend as average yield declined by 5bps to 15.8%. Buying interest was concentrated at the short end of the curve, particularly on the MAR-27 paper (-135bps), suggesting investors preference for shorter duration bonds. Meanwhile, mild sell pressure was recorded on the AUG-30 (+10bps), JAN-35 (+8bps), and AUG-34 (+7bps).

Similarly, the Eurobond market maintained its positive momentum, with average yield declining by 16bps to 6.9%, supported by sustained investor confidence and strong demand across the curve. Strong buying interest was seen in the FEB-30 (-22bps), FEB-38 (-19bps), SEPT-28 (-17bps), FEB-32 (-17bps), SEPT-33 (-17bps), and NOV-47 (-17b

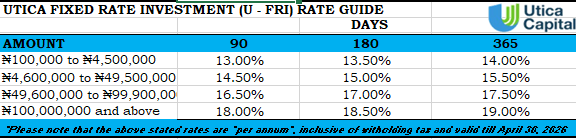

Fixed Income Opportunities for the week