Nigeria’s GDP Growth Hits 4.2%, Strongest in Four Years

Global Macro Highlights

US Records 3.8% Growth in Q2 2025, Fastest Since Q3 2023

The Bureau of Economic Analysis (BEA) reported that the US economy expanded by 3.8% YoY in Q2:2025, outperforming expectations and marking its fastest pace of growth since Q3:2023. The acceleration was driven primarily by resilient consumer spending, which rose by 2.5% (vs 1.6% in the prior quarter), reflecting steady household demand supported by consistent wage gains, accumulated savings buffers, and a strong labor market. Business investment also gathered pace, with notable growth in equipment (+8.5%) and intellectual property (+15.0%) as firms ramped up spending on automation, digital transformation, and Al-related upgrades.

The narrowing trade deficit-underpinned by falling imports services sector remained a key anchor of growth compared to the prior quarter where stockpiling of inventory ahead of the duties weighed on growth. Also, services growth, particularly in transport, finance, and insurance added further support.

Looking ahead, growth is expected to remain supported by firm consumer spending, higher government investment in green energy and infrastructure, and sustained corporate appetite for technology-driven investments. However, policy uncertainty, ongoing trade frictions, and labor supply constraints linked to immigration could weigh on momentum. In addition, tighter financial conditions, rising cost pressures, and a gradual cooling of labor demand are likely to temper activity. As such, we anticipate growth to moderate slight in the coming quarter.

U.S. Proposes Strict Rules to Curb Chip Import Dependence

The U.S. government is proposing new rules to compel semiconductor makers to boost domestic production. Under the proposal, chipmakers would need to produce in the U.S. an amount equivalent to what their customers import, with non-compliance potentially triggering tariffs of up to 100%. Companies already manufacturing domestically would be exempt, while those investing in new U.S. facilities could receive credits for pledged output, allowing temporary import flexibility until plants come online.

In our view, the policy could lift short-term costs for import-reliant firms, raising prices of electronics like smartphones, laptops, and household appliances, thereby adding to inflationary pressures. However, over the long run it could fortify U.S. semiconductor capacity, create jobs, and attract investment. Domestic chipmakers such as Intel and GlobalFoundries stand to benefit, while electronics producers may face margin pressures from higher component costs.

BOJ Faces More Pressure as Service Prices Edge Higher in August

Japan’s Services Producer Price Index (SPPI) rose by 2.7% YoY in August, up slightly from 2.6% in July, according to data from the Bank of Japan (BOJ). The hospitality sector remained the key driver, with hotel prices surging 7.6% (vs 5.4% in July), buoyed by robust inbound tourism following the complete removal of pandemic-era travel restrictions. Broader service categories also posted gains, reflecting persistent cost pressures across business- to-business services, largely from rising labor expenses in the region.

The continued uptick in the SPPI strengthens the BOJ’s case for further rate hikes as it works to align price levels more closely with its 2.0% inflation target.

Looking ahead, service-sector inflation is likely to remain elevated, supported by strong demand in tourism, hospitality, and business services, alongside resilient household spending and sustained wage growth. These dynamics provide the BOJ with room to cautiously advance its policy normalization agenda, while ensuring that its economic recovery is not derailed.

Global Equities Market

Weekly Performance of Major Global Indicies

Domestic Events

With Inflation Easing, CBN Moves to Loosen Financial Conditions

At its September 2025 meeting, the Monetary Policy Committee (MPC) cut the Monetary Policy Rate (MPR) by 50bps to 27.0%, marking the first rate reduction in five years. Alongside this, the Committee adjusted the asymmetric corridor to +250/-250bps, lowered the Cash Reserve Ratio (CRR) for deposit money banks to 45.0% (from 50.0%), retained the CRR for merchant banks at 16.0%, and maintained the Liquidity Ratio at 30.0%. In addition, the MPC newly introduced a 75.0% CRR on non-TSA public sector deposits as a liquidity management measure. The decision reflects improving domestic conditions: sustained disinflation with headline inflation easing to 20.1% in August (from 21.9% in July), stability of the Naira, and rising external reserves (at USD42.23bn). While the new 75% CRR requirement could moderate bank lending to the real sector, the overall policy stance is designed to ease financial conditions-supporting credit creation, lowering borrowing costs for businesses, while also maintaining stability in the FX market. Fixed-income yields may trend lower, while equities assets could benefit as investors reprice risk assets in light of improving macro fundamentals.

Nigeria’s GDP Growth Hits 4.2%, Strongest in Four Years

According to the National Bureau of Statistics (NBS), Nigeria’s GDP recorded its strongest quarterly performance in four years in Q2:2025, with GDP growth accelerating to 4.2% YoY from 3.1% and 3.5% in Q1:2025 and Q2:2024, respectively. The rebound was driven by a sharp recovery in the oil sector (+20.5% vs 10.1% in the corresponding period) as crude output rose to 1.68mbpd, supported by improved security, efficiency, and deepwater activity.

On the other hand, non-oil sector expanded by 3.6% (vs 3.3% in Q2:2024), supported by exchange rate stability, lower input costs, and steady interest rates. Services remained the largest contributor at 56.5% of total GDP, led by strong growth in telecommunications (+7.4% YoY), real estate (+3.8% YoY) and financial services (+16.2% YoY), while agriculture posted its best performance in three years at 2.8% due to higher crop production and better yields. Industry also strengthened, recording a 7.5% expansion compared to 3.7% a year earlier, thus increasing its GDP share to 17.3% from 16.8% in Q2:2024.

Nigeria’s growth outlook remains positive, supported by stronger oil production and steady gains in the agricultural sector. In addition, supportive government policies, a more accommodative monetary stance, and sustained Naira stability are expected to drive economic growth in the near to medium term.

NUPRC Approves $510mn Bonga Field Divestment Deal

The Nigerian Upstream Petroleum Regulatory Commission (NUPRC) has granted approval for a USD510mn divestment deal in the Bonga deepwater field, under which Total Energies will transfer its 12.5% contractor interest in Oil Mining Lease (OML) 118 to Shell Nigeria Exploration and Production Company (SNEPCO) and Nigerian Agip Exploration (NAE). According to the agreement, SNEPCO will acquire a 10.0% stake valued at USD408.0mn, while NAE will take up the remaining 2.5% for USD102.0mn. The transaction, however, remains subject to ministerial consent in line with the provisions of the Petroleum Industry Act (PIA), 2021.

In addition to the equity transfer, NUPRC emphasized that the acquiring parties – SNEPCO and NAE will assume full responsibility for decommissioning and abandonment, as well as host community commitments that was previously owed by TotalEnergies to the government. This reinforces the government’s push for accountability in environmental stewardship and community development within the oil and gas sector.

Beyond the immediate financial transaction, the deal highlights the broader restructuring currently underway in Nigeria’s upstream sector. International Oil Companies (IOCs) are increasingly reshaping their portfolios, focusing on strategic core assets while divesting from others. At the same time, regulators are ensuring that such exits do not leave behind unfunded liabilities or weaken host community protections.

Looking ahead, this deal is expected to strengthen Nigeria’s upstream sector by transferring OML 118 to experienced operators, reducing government liabilities, and aligning with the wider trend of IOC portfolio reshaping. However, sustained growth in the sector will hinge on the ability to strike a delicate balance between attracting investor confidence and meeting host community expectations.

Equities Market – Sectorial Performance

Weekly Performance of Sectorial Indices

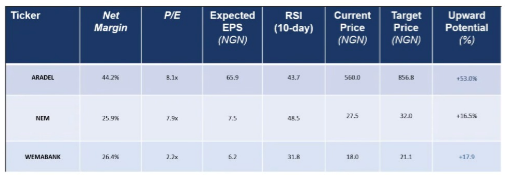

Stocks Top Picks for the Week

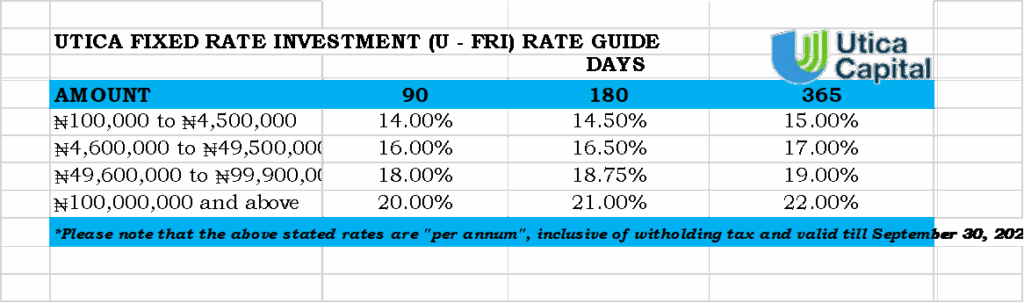

Fixed Income Opportunities for the week