MARKET UPDATE FOR THE WEEK 22ND JUNE

Global Macro Highlights

U.S. Federal Reserve Holds Rates Steady Amid Persistent Inflation

The Federal Reserve kept its benchmark interest rate unchanged at 3.50% -3.75% at its June meeting, marking the fourth consecutive meeting without a policy adjustment and the first under the new Fed Chair – Kevin Warsh. The decision was unanimous and widely expected, as inflation remains elevated at 4.2% (as of May 2026), way above the bank’s 2.0% target. Policymakers also moved away from earlier market expectations of imminent rate cuts and reiterated their commitment to returning inflation to target.

The decision points to growing caution from the Fed regarding the pace of inflation moderation. While economic growth remains resilient and labour market conditions are holding up, higher energy prices and supply disruptions linked to recent geopolitical tensions have slowed progress on inflation. Although the recent US-Iran peace agreement and the gradual reopening of the Strait of Hormuz is expected to ease pressure on global energy markets over time, policymakers appear unconvinced that inflation will decline quickly enough to warrant policy easing in the near term.

For financial markets, the implication is that interest rates are likely to remain elevated for longer than previously expected. Treasury yields may stay firm as investors reduce expectations for near-term rate cuts, while borrowing costs for households, businesses, and governments remain high. For businesses, particularly those reliant on debt financing, elevated funding costs could continue to weigh on investment and expansion plans. For households, higher mortgage, credit card, and consumer lending rates are likely to restrain spending. Equity markets may also face pressure from higher discount rates, although continued economic growth and stable corporate earnings should provide some support.

The Fed is expected to maintain its current policy stance in its upcoming meetings while closely monitoring inflation and labour market developments. Although easing tensions in the Middle East have reduced the risk of another major energy-driven inflation shock, inflation remains well above target. Unless there is a more meaningful decline in price pressures over the coming months, rate cuts are unlikely in the near term, while the possibility of an additional rate increase later this year remains on the table.

UK Inflation Steady at 2.8% as Underlying Price Pressures Persist

The Office for National Statistics (ONS) recently reported that UK’s headline inflation remained unchanged at +2.8% YoY in May 2026, indicating that overall price pressures have stabilized. On a monthly basis, consumer prices rose +0.2%, unchanged from the previous month. However, beneath the stable headline figure, underlying inflationary pressures remained firm with core inflation rising to +2.6% from +2.5%, driven largely by an increase in services inflation to +3.7% from +3.2%. Transport inflation also accelerated sharply to +6.8% YoY from +4.5% in April as higher fuel and transportation costs continued to filter through the economy following the energy market disruptions linked to tensions in the Middle East. These increases were partly offset by softer food and non-alcoholic beverage prices, preventing a broader rise in headline inflation. Consumer Prices Index including Owner Occupiers’ Housing costs (CPIH) inflation, also remained steady at 3.0%.

The data suggests that while headline inflation has somewhat stabled, underlying price pressures have not fully eased. In particular, services inflation remains elevated, indicating that domestic cost pressures, including wages and operating expenses, continue to keep inflation above the Bank of England’s (BOE) 2.0% target.

For households, stable inflation provides some relief after a prolonged period of rising living costs, although higher transport and service prices continue to weigh on disposable income. For businesses, especially those in transportation, hospitality, and service-related sectors, elevated operating costs are likely to persist, limiting the pace of margin recovery. For policymakers, the data reinforces the Bank of England’s cautious approach. While the stability in headline inflation reduces the urgency for further tightening, persistent core and services inflation make an immediate shift toward aggressive rate cuts unlikely.

We expect the BOE to hold rates in coming meetings, closely monitoring wage growth, labour market conditions, and energy prices. With inflation still above the bank’s target and underlying price pressures proving sticky, interest rates are likely to remain elevated for some time. However, we anticipate that easing energy market risks, following the US-Iran agreement, could reduce the likelihood of further rate hikes in the near term.

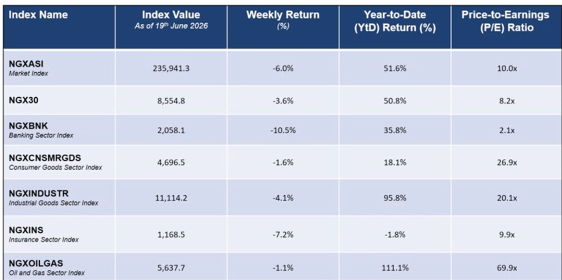

Global Equities Market – Sectorial Performance

Weekly Performance of Sectorial Indices

Domestic Events

Nigeria’s Inflation Rises for the Third Consecutive Month

Nigeria’s headline inflation rose to +15.93% YoY in May 2026 from +15.69% in April, marking the third consecutive month of acceleration. The increase was driven by higher food and core inflation, as planting season supply constraints, elevated transportation costs, and higher fuel prices continued to pressure consumer prices.

Although monthly inflation moderated during the month, inflation is expected to remain elevated in the near term, with lower global oil prices and a relatively stable exchange rate likely to support a gradual easing in price pressures.

NGX Introduces New Equity Pricing Framework to Boost Market Efficiency

The Nigerian Exchange (NGX) has introduced a new tiered equity pricing framework that reduces the volume required to move the prices of higher- priced stocks while retaining the existing threshold for lower-priced equities.

The change is aimed at improving price discovery, market efficiency, and liquidity by allowing stock prices to respond more quickly to changes in investor demand and supply.

Over time, the new framework is expected to enhance trading activity in premium stocks, although lower-priced equities may continue to experience relatively slower price adjustments.

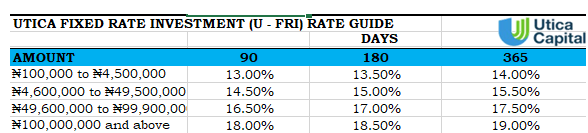

Fixed Income Opportunities for the week