MARKET UPDATE FOR THE WEEK 2ND JUNE

Global Macro Highlights

SARB Resumes Monetary Tightening as Inflation Risks Intensify

For the first time since 2023, the South African Reserve Bank (SARB) raised its benchmark repo rate, increasing it by 25bps to 7.0% at its May 2026 policy meeting as inflationary pressures re-emerged more aggressively than expected. Headline inflation accelerated sharply to 4.0% YoY in April from 3.1% in March, driven primarily by rising fuel and transport costs amid elevated global oil prices and persistent geopolitical tensions. Given South Africa’s position as a net fuel importer, the increase in energy prices has continued to feed directly into domestic inflation trajectory, pushing inflation back toward the upper bound of the SARB’s revised target range (3.0%).

Beyond the immediate fuel shock, the SARB’s latest decision mirrors growing concern that persistent supply-side pressures could begin to broaden into wider inflation expectations and core price pressures. The Bank highlighted several upside risks to inflation, including prolonged Middle East-related disruptions to global oil markets, weather-related food supply risks linked to El Niño conditions, and stronger pass-through effects from external shocks into domestic prices. Consequently, the SARB revised its inflation forecast upward to 4.4% ( vs 3.7%) for 2026 and 3.7% (vs 3.3%) for 2027, while lowering growth projections to 1.2% and 1.7% respectively, This revision is on the back of expectations that tighter financial conditions and weaker consumer purchasing power will weigh on domestic demand.

The rate hike is expected to keep borrowing conditions restrictive for households and businesses, likely moderating credit growth, consumption, and investment activity over the medium term. However, it also reinforces the SARB’s inflation-fighting credibility and supports investor confidence in South African fixed income assets amid heightened global uncertainty. Given the persistence of inflationary pressures and the upside risks from energy and food prices, we expect the SARB to maintain a tight monetary policy stance over the near term, with interest rates likely to remain elevated until there is clearer evidence of sustained moderation in inflation.

Global Equities Market – Sectorial Performance

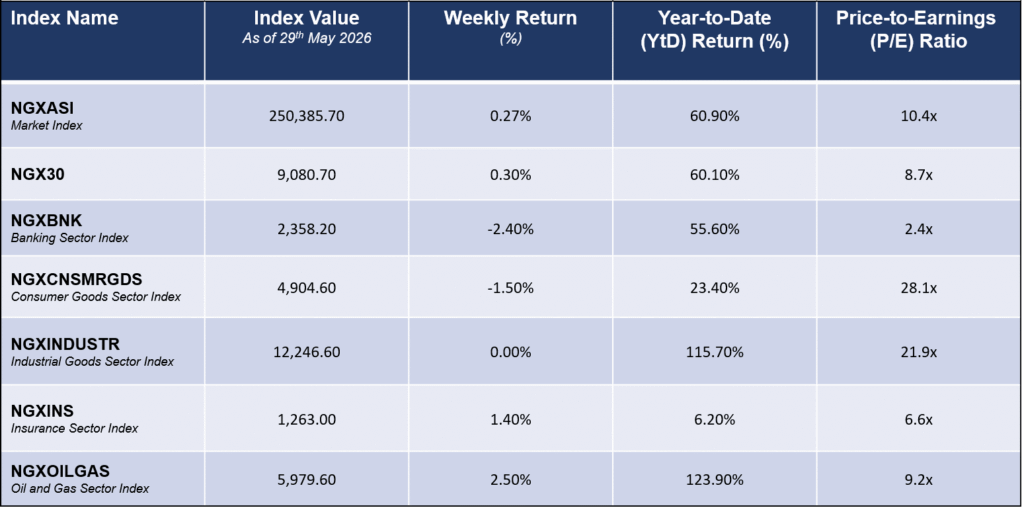

Weekly Performance of Sectorial Indices

Domestic Events

Nigeria Records Strongest First-Quarter Growth Since 2015

Data from the National Bureau of Statistics reveals the strongest first-quarter GDP growth since Q1:2015, at 3.9% in Q1:2026 (vs 3.1% in Q1:2025). This growth is supported by the non-oil sector, expanding 3.9% YoY, up from 3.2% YoY in Q1:2025, driven by strong performances across telecommunications (+12.2%), crop production (+3.4%), trade (+2.1%), real estate (+2.3%), and construction (+6.4%). Meanwhile, the services sector retained its top position in GDP composition at 57.7% (vs. 57.5% in Q1:2025), while agriculture and industry saw marginal share declines to 23.2% and 19.1%, from 23.3% and 19.2% in Q4:2024, respectively.

Despite a decline in oil production levels to 1.5mbpd (vs 1.6mbpd in Q1:2025), the oil sector also grew by +2.6% in Q1:2026 (vs 1.9% in Q1:2025). The improved growth relative to Q1:2025 was partly attributable to a low base effect and the solid performance of other oil sector activities, particularly gas production, which rose by +3.0% to 687,087.3mmscf in Q1:2026, partially cushioning the impact of lower crude oil production volumes during the period.

We expect the oil sector to sustain its growth trajectory, supported by improved security measures, faster reactivation of inactive wells, the commencement of FSO Cawthorne operations, and continued natural gas infrastructure developments, notably the completion of the OB3 pipeline’s River Niger crossing. Although, a high base effect from Q2:2025 is likely to moderate growth for oil sector in Q2:2026. On the non-oil side, we expect stronger growth momentum in Q2 2026, particularly on the back of sustained investment in the ICT sector, supported by rising data consumption, expanding broadband penetration, and continued digital adoption.

Nigeria Transitions to T+1 Settlement Cycle to Enhance Market Efficiency

Nigeria’s equities market is set for a major operational shift following the planned transition to a T+1 settlement cycle effective June 1, 2026. Under the new framework, equity transactions executed on the Nigerian Exchange will settle one business day after execution, compared to the current two-day timeline. The move marks an important step in modernising Nigeria’s post-trade infrastructure and brings the domestic market closer to evolving global settlement standards already adopted in several advanced markets. The transition is expected to improve market efficiency by reducing the time capital remain tied up after transactions. Faster settlement means investors can access cash and securities more quickly, enabling quicker portfolio rebalancing and reinvestment. The reform could be particularly beneficial for institutional and foreign investors, as shorter settlement timeline reduces counterparty and settlement risks while improving capital mobility. Over time, this may support stronger market participation and deeper liquidity in the equities market.

While some implementation challenges may emerge in the early stages as participants adjust to the faster timeline, the medium-term outlook remains positive. We believe a shorter settlement cycle should improve market efficiency, lower transaction risk, strengthen investor confidence, and enhance the competitiveness of Nigeria’s capital market within the global investment space.

Fixed-Income Market

The fixed income primary market was active during the week as the Central Bank of Nigeria (CBN) conducted an Open Market Operations (OMO) auction, offering NGN200.0bn across the 11-day, 39-day, and 102-day tenors. Investor demand remained concentrated at the longer end, with the 102-day instrument attracting the strongest subscriptions, signalling sustained preference for higher-yielding duration despite ongoing liquidity tightening.

Allotments were largely skewed toward the short and long tenors, while stop rates cleared at elevated levels above 20.0%.

In the Treasury bills secondary market, sentiment remained mildly positive, with average yields easing marginally to 17.5%. Buying interest was concentrated around mid-curve maturities, driving yield declines across selected papers, although profit-taking at the longer end partly offset gains and kept market movement relatively balanced.

The bond market, however, traded on a weaker note as average yields increased to 16.3%, driven by sell pressure across selected maturities following sharp gains recorded in the prior week. Despite the bearish undertone, selective demand in some instruments helped moderate the broader upward movement in yields.

In the Eurobond market, sentiment stayed supportive as sustained offshore demand compressed yields across tracked instruments, bringing average yields lower to 6.8% and highlighting continued investor appetite for Nigerian sovereign external debt.

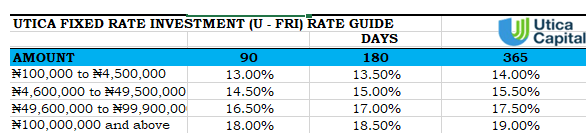

Fixed Income Opportunities for the week