Weekly Market Newsletter 8th April 2026

Global Macro Highlights

Euro Area Inflation Climbs as Energy Price Surge Intensifies Price Pressures

According to the statistical office of the European Union (Eurostat), inflation in the euro area rose for the second consecutive month to 2.5% YoY in March 2026 from 1.9% YoY in February, pushing inflation back above the European Central Bank’s (ECB) 2.0% target. The uptick largely reflects a renewed surge in energy prices, with energy inflation rising to 4.9% YoY from -3.1% in February – its first increase in nearly a year and the strongest since February 2023. The rebound in energy inflation stems from supply disruptions tied to escalating tensions in the Middle East, where damage to key infrastructure and constraints on oil logistics pushed global oil and gas prices higher. This quickly fed into domestic fuel costs, with sharp increases across Euro 95 (up 32.28% YoY and 34.98% MoM), diesel (up 56.08% YoY and 54.59% MoM), heating oil (up 49.83% YoY and 56.25% MoM), and LPG (up 3.58% YoY and 12.46% MoM).

While energy drove the headline increase, other components showed modest easing. Food, alcohol, and tobacco inflation edged down to 2.4% from 2.5%, while services slowed to 3.2% from 3.4%, suggesting some level of underlying stabilisation. On a monthly basis, headline inflation accelerated to 1.2% (from 0.6%), again reflecting the sharp turnaround in energy prices. Across the region, inflation pressures firmed broadly, with increases in Germany (2.8% vs. 2.0%), France (1.9% vs. 1.1%), Spain (3.3% vs. 2.5%), and the Netherlands (2.6% vs. 2.3%), while Italy remained stable at 1.5%. Smaller, more energy-dependent economies such as: Croatia (4.7% YoY vs 3.9%), Lithuania (4.5% YoY vs 3.3%), Luxembourg (3.8% YoY vs 1.8%), also recorded stronger price uptrend, further highlighting the widespread impact of the energy shock.

The March inflation figure shows that price pressures in the euro area could remain elevated in the near term, largely due to the recent jump in energy prices. Beyond keeping headline inflation high, this is likely to weigh on household purchasing power and consumer demand, while also raising input costs for businesses, potentially squeezing margins and slowing expansion. If sustained, higher energy cost are likely to filter into production, transport, and logistics, while rising fertilizer costs could also begin to push food prices higher. However, the pace of month-on-month increases may begin to moderate starting from next month, partly due to high base effect.

Against this backdrop, we expect the European Central Bank (ECB) to keep rates unchanged at its next meeting, allowing policymakers time to assess the persistence of recent inflationary pressures. With inflation edging higher, the focus is likely to remain on whether energy-driven increases begin to transmit into core inflation, as well as the extent to which elevated costs could weigh on growth and dampen consumer demand.

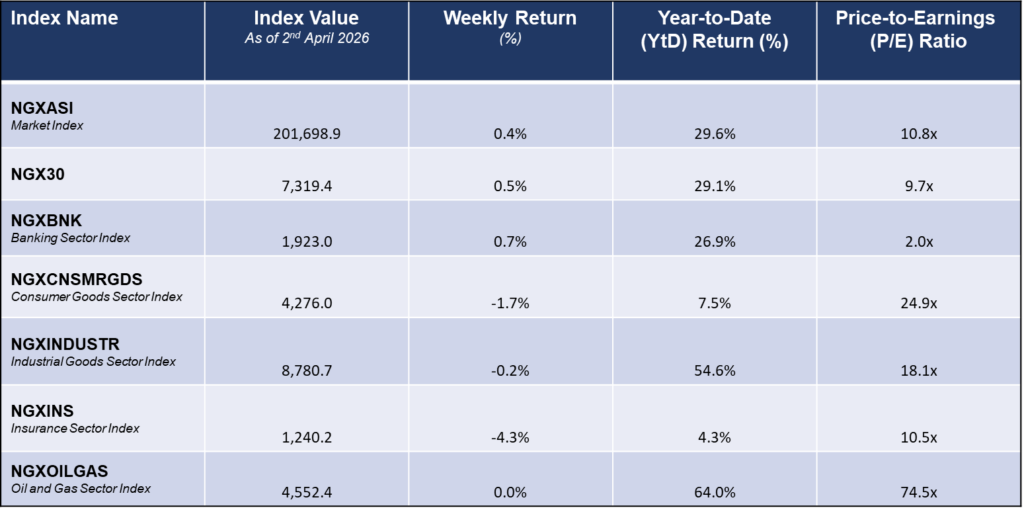

Global Equities Market – Sectorial Performance

Weekly Performance of Sectorial Indices

Domestic Events

House of Representatives Approves $6bn External Financing to Support Budget and Infrastructure Development

The House of Representatives recently approved the President’s request to secure USD6.0bn in external financing, comprising a USD5.0bn Total Return Swap (TRS) arranged with First Abu Dhabi Bank and a USD1.0bn export credit facility backed by UK Export Finance (UKEF) and arranged by Citibank, London. The TRS will be disbursed in tranches and is expected to support budget execution, fund critical infrastructure, and refinance relatively expensive domestic and external debt. Structurally, the facility will be backed by Naira-denominated bonds and require the government to make margin payments in US dollars if adverse price or FX movements reduce the value of the pledged securities below agreed thresholds. Meanwhile, the USD1.0bn facility would be allocated for the reconstruction of the Lagos Port Complex and Tin Can Island Port Complex, two of Nigeria’s most critical trade gateways. The arrangement provides a relatively fast channel for accessing external capital, providing near-term fiscal relief and supporting smoother execution of government spending plans, while also easing pressure on the domestic debt market. In addition, the planned upgrades to the two key ports are expected to improve trade flows and potentially stimulate broader economic activity over time. However, the transaction adds to Nigeria’s already elevated debt profile of NGN153.3trn as of September 30, 2025. Although the debt-to-GDP ratio improved to 37.9% in 2025 from 40.7% in 2024 on the back of stronger GDP growth, the additional borrowing is likely to have an adverse effect on debt metrics.

While the structure incorporates Naira-denominated interest payments, which helps limit direct foreign exchange risk on servicing costs, the transaction still introduces indirect FX exposure through the dollar-linked margin requirements under the TRS. As such, although improvements in port infrastructure could strengthen trade efficiency and support growth over the medium term, maintaining exchange rate stability will remain critical to ensuring that debt servicing risks remains manageable.

Nigeria’s Economy Sustains Broad-Based Expansion in March 2026

Data from the Central Bank of Nigeria (CBN) showed that Nigeria’s Purchasing Managers’ Index (PMI) came in at 53.2pts in March 2026, marking the sixteenth consecutive month of expansion, although slightly lower than the 56.4pts recorded in February. The expansion remained broad-based, with 31 subsectors recording growth, led by the Electrical Equipment segment, while five subsectors contracted, with Primary Metals posting the steepest decline. Sectoral performance remained positive across the board, with the Industry sector leading at 54.0pts, supported by stronger new orders and increased manufacturing output, particularly from rising demand for electrical equipment driven by a shift toward alternative power sources and growing investment in renewable and digital infrastructure. The Agriculture sector posted 52.8pts, extending its expansion streak to twenty consecutive months, driven by resilient farming activities and sustained growth in key staples. Similarly, the Services sector recorded 52.0pts, marking its fourteenth month of expansion, with the Education subsector driving growth alongside steady improvements in overall business operations. Meanwhile, the employment index rose to 52.2 points, representing continued hiring as firms scale up capacity to meet demand.

Overall, the data points to a sustained, albeit moderating, expansion in economic activity, with firms continuing to ramp up production and employment in response to resilient demand. This supports a positive outlook for Q1:2026 GDP growth, as higher business activity typically translates into increased output. Economic conditions are expected to remain relatively stable, with activity likely to stay in expansionary territory in the near term.

Fixed-Income Market

In the primary fixed income market, the CBN conducted two OMO auctions during the week. At the first auction held on Monday, the CBN offered NGN600.0bn across the 8‑day, 99‑day, and 120‑day tenors. Investor demand softened, with total subscriptions declining by 31.8% to NGN1.9trn, resulting in a subscription‑to‑offer ratio of 3.2x. The CBN ultimately allotted NGN1.7trn, translating to a bid‑to‑cover ratio of 2.9x. Stop rates cleared at 21.9% (8‑day), 19.8% (99‑day), and 19.9% (120‑day).

At the second auction on Tuesday, the CBN offered NGN600.0bn, this time across the 70‑day and 140‑day maturities. Demand weakened further, with subscriptions falling by 33.4% to NGN1.3trn, representing a subscription‑to‑offer ratio of 2.2x. Total allotment settled at NGN853.8bn, with a bid‑to‑cover ratio of 1.4x. Stop rates for both the 70‑day and 140‑day instruments cleared at 19.9%.

Meanwhile, the Debt Management Office (DMO) held its monthly FGN bond auction, offering NGN750.0bn through reopening of the JUN‑32, MAY‑33, and FEB‑34 issues. Investor appetite moderated sharply, with total subscriptions dropping to NGN931.5bn, compared with NGN2.7trn in February 2026. Consequently, total allotment declined to NGN485.5bn, from NGN524.3bn at the prior auction. Stop rates rose across all maturities, with the JUN‑32 clearing at 16.0%, MAY‑33 at 16.2%, and FEB‑34 at 16.6%. This moderation in demand could be linked to investors cautious sentiment amid inflation concerns, which weighed on duration appetite and pushed pricing higher.

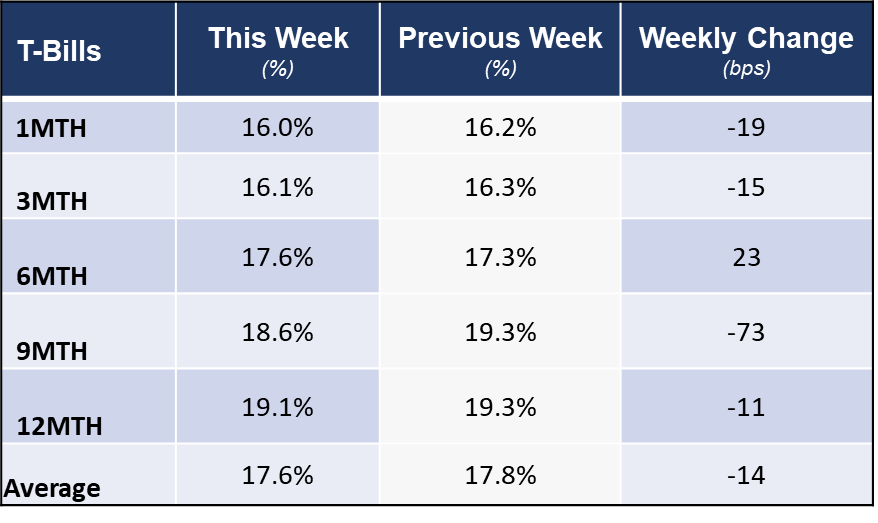

The secondary T‑bills market reversed its bearish trend, with average yield declining by 14bps to 17.6% from 17.8% the previous week. Renewed interest was noticed across the curve, with major contractions on the DEC‑26 (-95bps), JAN-27 (-52bps), MAR-27 (-36bps), and OCT‑26 (-30bps) maturities. Meanwhile, sell pressure was observed on the APR‑26 (+30bps) and SEPT‑26 (+22bps) bills.

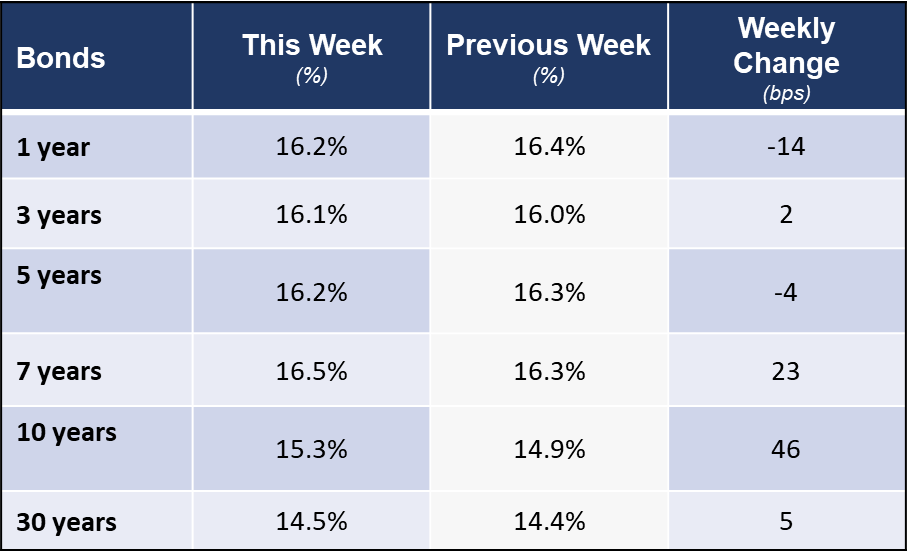

In contrast, the secondary bond market extended its bearish run, with average yields edging up by 1bp to 15.8%. Selling pressure remained concentrated around the belly of the curve, particularly on the MAY-33 (+33bps), JUN-33 (+28bps), FEB-34 (+21bps), and JAN-35 (+13bps) issues, suggesting weak investors’ appetite for duration amid inflation concern. Nonetheless, mild buying interest was observed on the JAN-42 (-27bps) and JUL-45 (-14bps) bonds.

Meanwhile, sentiment in the Eurobond market turned bullish, with average yield declining by 2bps to 7.5%, driven by broad-based demand across the curve. The strongest buying interest was seen on the JAN-49 (-16bps), SEPT-51 (-13bps), and NOV-47 (-11bps) issues, while only the JAN-31 (+18bps), and FEB-30 (+13bps) recorded sell-offs.

Market Snapshot

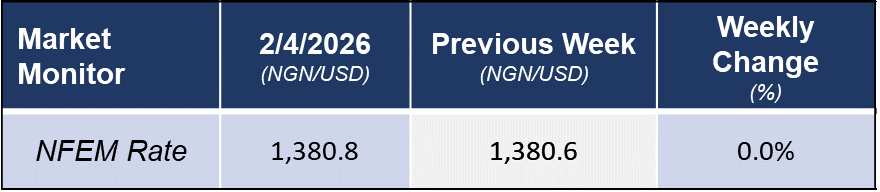

FX Monitor

Secondary Market Monitor

Money Market Rates

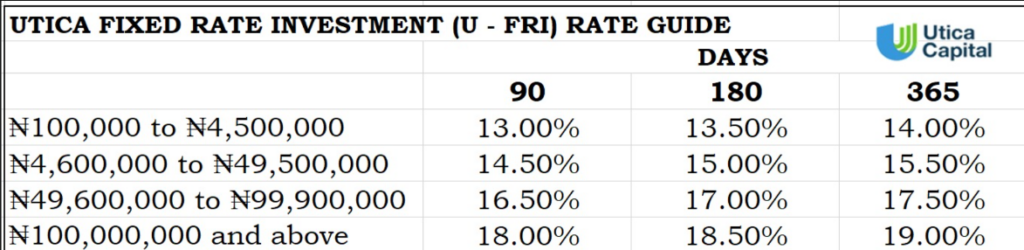

Fixed Income Opportunities for the week