Global Macro Highlights

Euro Area Records Moderate Growth in Q4 2025 as Household Consumption Strengthens

According to Eurostat, economic activity in the euro area expanded modestly in the final quarter of 2025, with GDP rising by 0.2% in Q4:2025, a slight moderation from the 0.3% growth recorded in Q3:2025, while labour market conditions remained resilient during the period. On a year-on-year basis, the euro area economy expanded by 1.2% in Q4:2025. The expansion was largely supported by stronger household consumption, which increased by 0.4% QoQ, from 0.2% in the previous quarter, supported by the combined effect of a resilient labour market (with number of employed persons rising by 0.2% during the quarter), continued wage growth, and seasonal spending during the festive period. Additional support came from government consumption, which increased by 0.5% QoQ (vs 0.7% QoQ) and gross fixed capital formation, which rose by 0.6% QoQ (vs 1.3% QoQ), although both components grew at a slower pace compared with the previous quarter. In contrast, net trade weighed slightly on overall output as it declined by 0.1% QoQ, primarily due to a 0.4% QoQ contraction in exports following headwinds from weaker global trade and heightened geopolitical uncertainty.

Across the euro area’s largest economies, growth performance remained uneven. Spain recorded the strongest expansion with GDP increasing by 0.8% QoQ (vs 0.6% QoQ in Q3:2025), driven largely by robust household and business spending. This was followed by the Netherlands (0.5% QoQ), while Germany and Italy recorded more moderate growth of 0.3% QoQ, and France posted a smaller increase of 0.2% QoQ. The latest GDP figures point to gradual but positive economic momentum across the region, suggesting that the euro area continues to expand at a measured pace despite subdued investment activity and lingering external uncertainties, developments which is likely to strengthen investor confidence and support capital allocation.

Looking ahead, domestic demand is expected to remain the primary driver of economic activity across the euro area. Rising real incomes and a gradual decline of excess household savings are likely to sustain consumer spending, while resilient labour market conditions should continue to support household demand. Although geopolitical risks and global trade uncertainties remain key downside risks, planned public investment programmes across several member states are expected to provide additional support to economic activity. At the same time, a relatively strong euro could continue to weigh on export competitiveness, potentially limiting the pace of overall expansion which is likely to keep growth across the euro area moderate in the near term.

Moderate Rise in Euro Area Inflation Keeps Price Pressures Near ECB Target

According to Eurostat’s flash estimate, Euro area annual inflation is estimated to have risen slightly to 1.9% YoY in February 2026, from 1.7% recorded in January 2026. The evaluation suggests a modest rebound in price pressures across the bloc after several months of gradual disinflation. Despite the modest increase, inflation is still hovering around the European Central Banks (ECB’s) 2.0% target, proving that price pressure across the region remains broadly in control.

Looking at the drivers of the February estimate, the flash data shows that services inflation remains the largest contributor, with prices estimated to have increased to 3.4% in February from 3.2% in January. The increase reflects persistent wage pressures and strong demand in service-related activities, including tourism, hospitality and transport. Food, alcohol and tobacco prices also valued at 2.6% in February, compared with 2.5% in December and 2.6% in January. Within this category, unprocessed food inflation is projected to have moved sharply to 4.6% YoY in February (vs 4.2%), suggesting that fresh food prices (often affected by weather patterns and supply disruptions) played a role in pushing the overall reading slightly higher.

In contrast, energy inflation is assessed to remain negative at -3.2% in February, although this represents a slight improvement from -4.0% in January. This suggests that while energy costs are still falling on a year-on-year basis, the pace of decline is beginning to moderate. The continued weakness in energy inflation largely shows a more stable global energy markets and lower wholesale gas prices. Similarly, non-energy industrial goods inflation remains relatively subdued, with prices estimated to have increased by 0.7% in February, up from 0.4% in January. The relatively low inflation in this category reflects improving supply chain conditions and the impact of a stronger euro, which has helped reduce the cost of imported manufactured goods. Looking at inflation across individual euro area economies, the preliminary data shows that Slovakia is estimated to have recorded the highest annual inflation rate at 4.0% in February 2026, slightly lower than 4.3% in January, but still well above the euro area average of 1.9%. While, Cyprus is estimated to have recorded the lowest inflation rate in the euro area at 0.9%, down from 1.2% in January.

In terms of economic impact, the slight increase in inflation does not necessarily signal a return of strong price pressures. The headline rate is still estimated to remain below the ECB’s 2% target, thereby, for households, the continued decline in energy prices (-3.2%) helps offset some of the cost pressures from food and services. For businesses, the relatively low inflation in non-energy industrial goods (0.7%) and stable input prices could support operating margins and investment planning. Looking ahead, euro area inflation is expected to remain cautiously balanced, especially given that this figure is based on preliminary estimates and may be revised when the final data is released. That said, current trends suggest that inflation is likely to remain around the ECB’s target in the near term, supported by subdued energy prices and easing goods inflation. However, services inflation and wage growth will remain key variables to watch, as sustained pressure in these areas could slow the pace at which inflation fully stabilises.

Escalating Iran Conflict Disrupts Oil Markets and Raises Global Economic Risks

The conflict involving the U.S., Israel, and Iran escalated sharply on 28 February 2026, when the U.S. and Israel launched coordinated air and missile strikes on Iranian military infrastructure and nuclear-related facilities, killing Iran’s Supreme leader, Ali Khamenei. The attack formed part of a broader military escalation after weeks of tensions over Iran’s nuclear programme and missile development. In retaliation, Iran launched missile and drone strikes on multiple U.S. bases across the Middle East, including Saudi Arabia, Jordan, Lebanon and Iraq. These attacks disrupted shipping and energy infrastructure around the Strait of Hormuz, a key global oil shipping route for Asia pacific economies like China. As a result, global oil prices spiked, with Brent Crude climbing by +8.4% to USD79.4pb from USD73.2pb before easing to USD77.2pb and later surging to USD84.80pb after the IRGC declared the strait “closed” and threatened any vessel attempting passage.

A prolonged conflict could trigger renewed global inflation, particularly through higher energy costs (which had been a key driver of moderating inflation in recent months) and food prices (with higher fertilizer costs pushing up prices of staples such as wheat, corn, and soybeans). Higher inflation may force central banks to delay further monetary easing and adopt a more cautious stance. For corporates, prolonged conflict could raise input costs, compress margins, and weaken earnings performance, potentially triggering risk‑off sentiment in equity markets and a rotation toward safe‑haven assets.

For Nigeria, the shock presents both upside and downside risks. Given the country’s heavy dependence on crude exports, elevated oil prices would support trade performance, strengthen export receipts, improve FX liquidity and trade balances and government revenues (particularly with oil now trading above the 2026–2028 MTEF benchmark of USD64.9/pb). However, higher global oil prices pose inflation risks for the now deregulated downstream market, as the recent price surge has already led to upward adjustments by downstream operators. These pressures could prompt a renewed uptick in month‑on‑month inflation and may delay any further rate cuts by the Monetary Policy Committees. For market, foreign outflows may increase as global investors reduce exposure to emerging markets in favour of safe‑haven or less riskier assets.

In the near term, oil prices are likely to remain elevated. However, ongoing diplomatic efforts—particularly China’s pressure on Iran to keep energy flows open, and the U.S. offer of naval escorts and government‑backed shipping insurance—are likely to contain the conflict and help stabilize oil prices over the medium to long term.

Global Equities Market – Sectorial Performance

Weekly Performance of Sectorial Indices

Domestic Events

CBN Expands Gold Reserves to $3.5bn in Push for Reserve Diversification

The Central Bank of Nigeria (CBN) has increased its gold holdings to about USD3.5bn, reflecting a gradual shift in how the country manages its external reserves. The increase is largely tied to the CBN’s domestic gold purchase programme, which allows the central bank to buy gold produced locally and add it to Nigeria’s reserve assets.

This development reflects the continued implementation of the National Gold Purchase Programme (NGPP), a policy initiative introduced in 2020 to strengthen reserve diversification and formalise the country’s artisanal gold mining sector. Under this programme, the CBN purchases gold from licensed miners and refiners within the country. The gold is refined to international standards and then acquired in naira before being recognised as part of Nigeria’s official reserves in dollar terms. This approach allows the central bank to build reserves without directly spending foreign currency, while also supporting activity in the local mining sector.

A key motivation behind this strategy is the growing need to diversify reserve assets. Historically, Nigeria’s reserves have been heavily concentrated in foreign currencies, particularly the US dollar. Gold, however, tends to retain its value during periods of global uncertainty, which is why many central banks have been increasing their allocations to the asset in recent years. In Nigeria’s case, the expansion of gold reserves underscores both continued purchases and the benefit of relatively strong global gold prices. Beyond strengthening reserves, the programme could also support the broader economy activity. By acting as a steady buyer of locally produced gold, the CBN helps encourage formal mining activity and better regulation within the sector, particularly among small-scale miners. Over time, this could help deepen Nigeria’s mining industry and contribute to export diversification, an area the country has been trying to develop beyond oil.

From a macroeconomic perspective, stronger and more diversified reserves can help reinforce confidence in the external sector, especially during periods of exchange rate pressure. A healthier reserve buffer generally gives the central bank more flexibility to manage liquidity in the foreign exchange market when needed. Looking ahead, the pace of further accumulation will likely depend on domestic gold production, global gold prices, and the CBN’s broader reserve management strategy. If the programme continues and local mining capacity improves, Nigeria could gradually increase the share of gold within its reserves, strengthening its external buffers over time.

Fixed-Income Market

The fixed income market was a buzz of activity with the CBN conducting two OMO auctions, along with its scheduled Treasury bill auction. At the first OMO auction, the CBN offered NGN600bn across the 8‑day, 99‑day, and 106‑day maturities. Investor demand weakened sharply, with total subscriptions dropping 58.8% from the previous auction to NGN979.6bn, bringing the subscription‑to‑offer ratio to 1.63x. Total allotment fell well below the offer at NGN256.0bn, translating to a 0.4x bid‑to‑cover ratio. Stop rates were set at 19.4% for the 99‑day and 19.4% for the 106‑day papers, while no allotment was made on the 8‑day bill. At the second OMO auction, the offer size remained NGN600bn across the 7‑day, 98‑day, and 105‑day instruments. Subscriptions declined further by 27.3% to NGN711.9bn, with demand heavily skewed toward the 105‑day tenor, accounting for 97.9% of total bids. The CBN allotted NGN235.6bn, resulting in a 0.4x bid‑to‑cover ratio. Stop rates were unchanged at 19.4% for the 98‑day and 19.4% for the 105‑day instruments, and again, the 7‑day bill recorded no sales.

At the first T‑bills auction in March, the CBN offered NGN1.1trn across the 91‑day, 182‑day, and 364‑day tenors. Investor demand moderated by 45.3% to NGN2.3trn (from NGN4.3trn previously), while total allotment dropped to NGN1.0trn from NGN1.9trn at the last auction. The bid‑to‑cover and subscription‑to‑offer ratios stood at 0.9x and 2.2x, respectively. Stop rates increased on the 91‑day (to 15.9% vs 15.8%) and 364‑day (to 16.7% vs 15.90%), while the 182‑day tenor held steady at 16.6%.

In the secondary T-bills market, sentiment turned bearish as average yields climbed by 26bps to 17.5% from 17.2% in the prior week, as investors reacted to the upward repricing at the primary auction. Sell‑offs were pronounced at the long end, particularly on the FEB-27 (+85bps), NOV-26 (+67bps), SEPT-26 (+59bps) and JAN-27 (+48bps) maturities. Gains at the short‑to‑mid segment were not enough to offset the broader weakness.

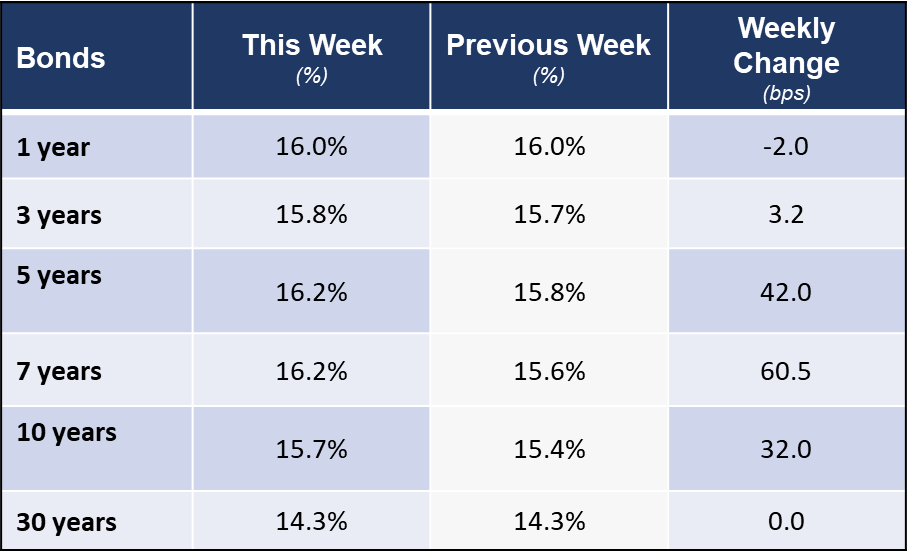

The secondary bond market also reversed earlier gains, closing the week bearish as average yields rose by 20bps to 15.7% from 15.5%. Sell‑offs were concentrated at the belly of the curve, with major moves on the FEB-34 (+85bps), JUL-34 (+62bps), MAR-35 (+61bps), MAY-33 (+57bps) and APR-32 (-56bps) papers. Only a few bonds, such as APR-29 (-8bps), MAR-27 (+5bps), MAR-28 (-3bps) and JUN-38 (-1bps) attracted buying interest.

The Eurobond market followed the same bearish pattern, with average yields increasing by 19bps to 7.2%, driven by risk‑off sentiment stemming from renewed geopolitical tensions involving the U.S., Israel, and Iran. The sell‑off was broad‑based, with the NOV-27 (+30bps), SEPT-33 (+29bps), JAN-31 (+24bps) and FEB-32 (+23bps) notes recording the most significant yield increases.

Market Snapshot

FX Monitor

Secondary Market Monitor

Fixed Income Opportunities for the week