Nigeria Strengthens Healthcare Through Strategic US & EU Partnerships

Global Macro Highlights

UK Growth Slows Amid Weak Demand

According to the U.S. Bureau of Economic Analysis (BEA), the U.S. economy expanded at an annualised rate of 4.3% in Q3:2025, up from 3.8% in Q2:2025, the strongest growth rate in several quarters. The main driver of this growth was consumer spending which rose by 3.5% (the fastest pace this year), on the back of goods (+3.10%) and services (+3.7%), with particularly strong demand in healthcare, professional services, and leisure activities.

Exports rebounded sharply, rising by 8.8%, after falling 1.8% in the previous quarter, driven mainly by capital goods and non-durable goods, reflecting stronger global demand and more stable supply chains. At the same time, imports fell by 4.7%, as domestic demand for imported goods softened. Together, this meant that net exports made a positive contribution to GDP growth. Government consumption increased by 2.2%, after contracting 0.1% in Q2. This reflects higher federal and state spending, including defense and public services, which provided an additional boost to growth.

Private investment was mixed, as fixed investment (+1.0%) held up at a slower pace, supported by equipment and intellectual property products, while investment in structures (-6.3%) and residential (-5.1%) remained constrained by elevated mortgage rates. On the production side, services remained the primary growth driver, while manufacturing activity stabilised following earlier weakness. Overall, Q3:2025 GDP points to an improving expansionary growth trajectory.

Looking ahead, growth is expected to moderate into late 2025, mainly because the third quarter was already very strong, not because the economy is slowing sharply. Toward the end of 2025, consumer spending is likely to ease slightly as households run down savings and the labor market cools gradually. In 2026, growth should remain steady, helped by lower inflation and the likelihood of further interest rate cuts, which should support investment over time.

UK Growth Loses Momentum as Domestic Demand Remains Fragile

On a year-on-year basis, the UK economy expanded by 1.3% in Q3:2025, slightly below 1.4% in Q2:2025, according to the Office for National Statistics. On a quarterly basis, growth slowed to 0.1% in Q3:2025, in line with the preliminary estimate, from 0.2% in Q2:2025 (revised down from 0.3%), this weaker momentum came despite a modest uptick in household consumption. On the production side, growth moderated to 0.3% QoQ from 0.8% in Q2:2025, weighed down by contractions in manufacturing (-0.8%) and mining and quarrying (-0.4%). Services growth slowed to 0.2% QoQ from 0.4%, driven by gains in financial and real estate activities, but partially offset by declines in professional and technical services. Construction expanded by 0.2% QoQ, supported by repair and maintenance activity.

There were a few positives, business investment rebounded by 1.5% QoQ in Q3:2025 from -1.1% in Q2:2025. Government spending increased by 0.4%, while household consumption rose by 0.3%, although at a slower pace than in the previous quarter. Overall, the slowdown points to fragile domestic demand and an economy operating close to stall speed, increasing sensitivity to shocks and limiting policy flexibility. We expect growth to remain weak in Q4:2025, in line with the Bank of England’s projection of flat output, as domestic demand continues to be constrained. While household consumption should receive temporary support from festive season demand, elevated borrowing costs and still-tight financial conditions are expected to limit discretionary spending and housing activity. Easing inflation should support real income dynamics, although the pass-through is likely to be gradual and insufficient to drive a near-term rebound in demand. Business investment is expected to remain cautious amid subdued confidence and policy uncertainty around taxes, while external demand remains soft. Labour market resilience and targeted fiscal spending should help cushion downside risks, but are unlikely to generate a material acceleration in activity. Any recovery into 2026 is likely to be gradual and dependent on a sustained easing in financial conditions and a clearer improvement in real income growth.

Global Equities Market

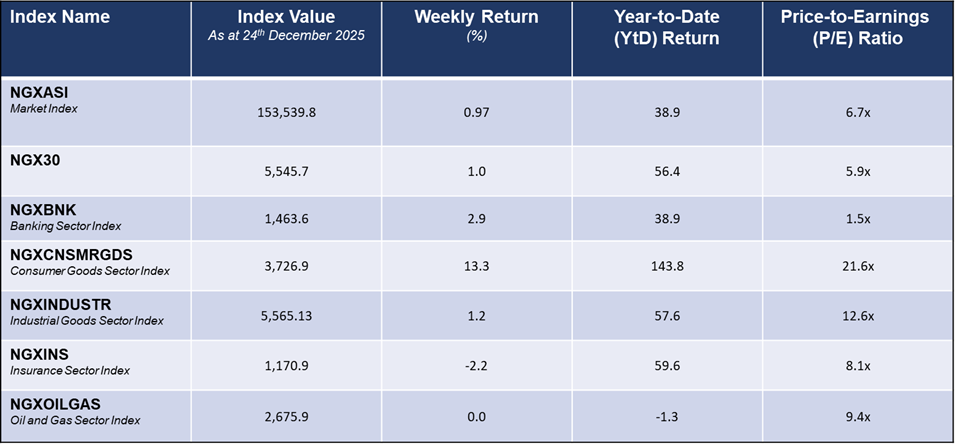

Weekly Performance of Major Global Indices

Domestic Events

Nigeria Strengthens Healthcare Through Strategic US & EU Partnerships

The Federal Government of Nigeria has signed a five-year memorandum of understanding (MOU) with the United States to advance the America First Global Health Strategy. The agreement covers a USD5.1bn bilateral health framework, comprising USD2.1bn in U.S. health assistance and a USD3.0bn domestic funding commitment from Nigeria, which should translate into a material expansion of Nigeria’s healthcare budget. The MOU is structured to strengthen domestic health expenditure with particular focus on Christian faith-based healthcare providers, while also building system resilience and expanding access to essential services for malaria, polio, and maternal and child healthcare. This is also expected to reinforce Nigeria–U.S. diplomatic and development cooperation. This development follows an earlier agreement signed in October 2025 with European Union partners, which focuses on healthcare financing, pharmaceutical supply-chain expansion, and support for universal health coverage through local manufacturing of essential drugs to reduce import dependence.

Taken together, these agreements signal a strategic shift toward a multi-partner approach to healthcare reform in Nigeria. The EU partnership addresses structural and financing constraints within healthcare delivery, while the U.S. MOU complements this through technical expertise, innovation, and disease-control . support. Combined, these partnerships should accelerate progress toward sustainable healthcare development, strengthen resilience against future health shocks, and support a more integrated global healthcare framework.

Fidson Healthcare Launches NGN21bn Rights Issue to Fund Growth and Reduce Debt

Fidson Healthcare Plc has announced plans to raise NGN21.0bn through a Rights Issue, offering 600mn ordinary shares at a fixed price of NGN35.0 per share. The offer is structured as one new share for every four shares held, based on shareholders on record as of November 12, 2025. The offer opened on December 19, 2025, and will close on January 30, 2026.

The offer price represents a 10.3% discount to the market price of NGN39.0 on the qualification date and an even wider discount to the current share price of NGN43.9, giving existing shareholders the chance to increase their holdings at a relatively attractive valuation. Proceeds from the Rights Issue will be used mainly to strengthen the balance sheet and support growth. Fidson plans to allocate about NGN7.5bn to capital expenditure, NGN9.5bn to reduce debt, and NGN3.5bn to working capital needs. However, borrowings have increased by about 23.8%YoY, rising to NGN19.8bn from NGN16.0bn as of 9M:2024, largely due to ongoing expansion.

By using part of the proceeds to pay down debt, Fidson should benefit from lower interest costs, which would help improve profitability, cash flow, and overall financial flexibility over the medium term. Overall, the Rights Issue places Fidson in a better position to pursue sustainable growth while managing balance sheet risks. For investors, the discounted pricing offers an attractive opportunity to increase exposure, while the planned use of funds supports both deleveraging and capacity expansion. Over the longer term, successful execution of these plans, alongside Fidson’s international partnerships aimed at boosting local pharmaceutical manufacturing, should strengthen its competitive position and support shareholder value.

Fixed Income Market

At the OMO auction held during the week, investor demand remained very strong, with total subscriptions reaching NGN2.4trn against the NGN600bn offered by the CBN. Demand was largely concentrated in the longer 211-day tenor, which attracted NGN1.9trn in bids. The CBN allotted NGN1.7trn in total, resulting in a bid-to-cover ratio of 1.37x and a bid-to-offer ratio of 3.93x. Stop rates settled at 19.4% on the 162-day bill and 19.4% on the 211-day bill.

In the secondary market, treasury bill yields moved higher, reversing the bullish trend seen in recent weeks. The average yield increased by 4bps to 17.8%, driven mainly by selling pressure in shorter-dated bills. The sharpest increases were recorded on the 11-Jun-26 (+62 bps), 12-Mar-26 (+45 bps), and 5-Feb-26 (+38 bps) maturities. This more than offset continued demand for longer-dated bills, where yields declined on the 19-Nov-26 (-31 bps) and 17-Dec-26 (-24 bps) papers.

In contrast, the secondary bond market turned positive after four consecutive weeks of weakness. Average bond yields declined by 5bps to 16.7%, supported by buying interest in the short to mid sections of the curve. Notable yield declines were seen on the JAN-35 (-31 bps), JUL-34 (-24 bps), and MAR-27 (-23 bps) bonds. This buying interest outweighed modest sell-offs in some longer-dated bonds, including the JUN-32 (+13 bps) and MAY-33 (+12 bps). Meanwhile, the Eurobond market extended its rally for a second consecutive week. Average yields fell by 6bps to 7.0%, compared with 7.1% in the previous week. The gains were broad-based, with the largest moves seen on the FEB-30 (-12 bps), SEP-33 (-11 bps), and MAR-29 (-8 bps) tenors.

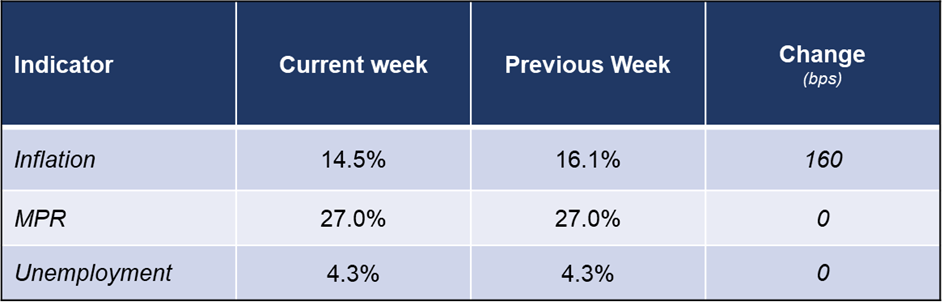

Macroeconomic Indicators

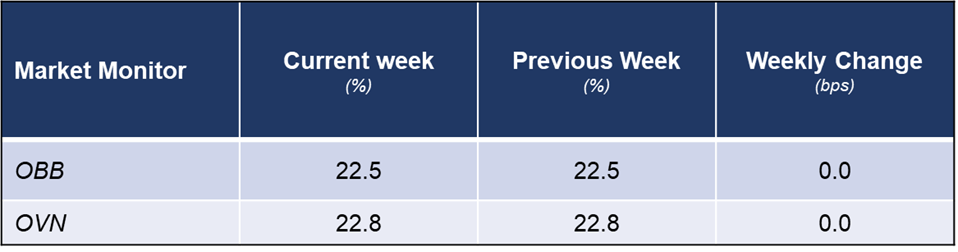

Money Market Rates

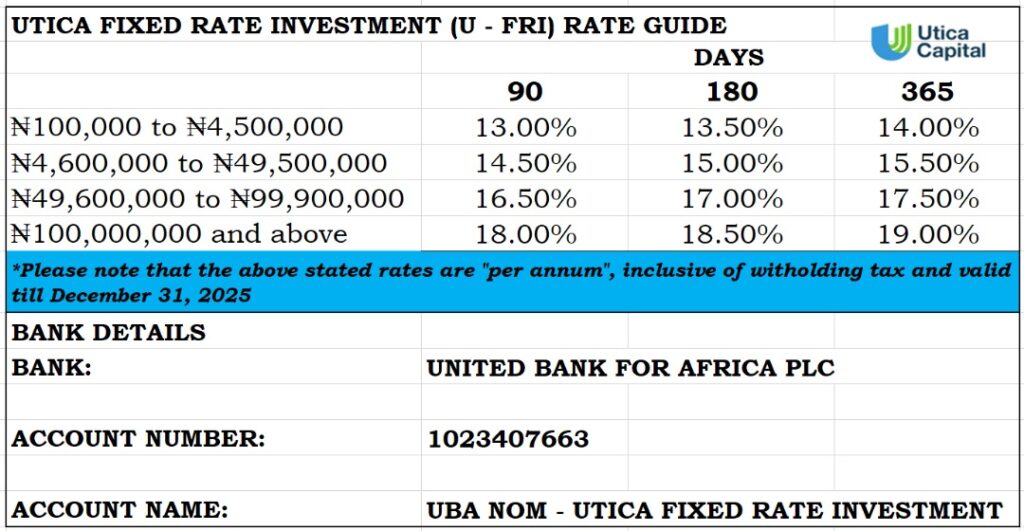

Fixed Income Opportunities for the week