Nigeria’s Currency in Circulation Growth Slows, Reflecting Tighter Liquidity and Rising Digital Payment

Global Macro Highlights

BOE Holds Rates at 4%, Weighing Inflation, Wages, and Fiscal Uncertainty

The Bank of England (BOE) kept the Monetary Policy Rate unchanged at 4.0%, marking two consecutive meetings with a hold decision. The policymakers noted that cutting rates too soon could risk reversing the recent progress on prices, especially with wage growth still elevated and the labour market showing mixed signals. The decision also factored in uncertainty around the government’s upcoming budget, which could alter the near-term fiscal stance and influence demand conditions. For now, maintaining the current rate gives the Bank room to assess the pace of inflationary pressure (inflation held steady at 3.8% since July, however, still above the 2.0% bank’s target)

Looking ahead, the policy path will depend on how quickly inflation continues to ease, the direction of wage pressures, and the fiscal signals that emerge from the next government statement. A modest cut before year-end remains possible if disinflation gains traction and domestic demand stays soft. However, any renewed price pressure or firmer labour-market data could shift easing into early 2026. Overall, the Bank is trying to secure a clear path back to target inflation without placing additional strain on an economy that is only gradually recovering.

Eurozone Economy Expands in October, Services Drive Strongest Growth Since May 2023

The Eurozone economy witnessed an expansion in October with its Composite Purchasing Managers’ Index climbing to 52.5 compared to 51.2 in September. The expansion also marks the 10th consecutive month of growth, reaching its highest level in 29 months. The expansion was driven by a sharp acceleration in services activity, which expanded to 52.6 in October vs 51.3 in September, a new one-year high. The manufacturing output edged slightly to finish at 50.0 vs 49.8 in September. Stronger domestic demand buoyed the recovery as new business rose at the fastest pace in two and a half years, signalled by the new orders index, which jumped to 52.1 from 50.6.

This impacted businesses positively as firms increased their staffing, causing employment growth to accelerate to a 16-month high, even as firms’ expectations for future activity softened marginally. Consequently, the service activity index increased to 53.0 from September’s 51.3, reaching a 17-month high. The expansion signals the strongest since May 2023, and a gradual rebound from the subdued growth we have seen in 2025 brought about slowing demand, consumer confidence and consumption, and the uncertainties and disruptions to trade initially by the U.S. tariffs.

Going forward, we expect the expansion to continue in the short term buoyed by increasing consumer demand during the holiday season, and an expansion in the service index which is expected to receive support from a wide range of holiday activities. Also, the winter season may drive demand upwards for apparel and clothing. This would positively impact employment. Overall, we expect the Eurozone economy to continue to rebound in 2026.

Ghana Inflation Eases to 8% in October, Lowest in Over Four Years

Ghana’s disinflationary trend extended into October 2025, with headline inflation easing to 8.0% YoY from 9.4% YoY in September 2025. This is the lowest level in over four years and remains broadly in line with the Bank of Ghana’s 6.0%-10.0% target band. This decline was driven mainly by softer food prices, with food inflation easing to 9.5% from 11.0%, while non-food inflation slowed to 6.9% from 8.2%, supported by a more stable macro environment, tighter fiscal discipline under the IMF programme, and a stronger cedi, which has appreciated by nearly 34.5% year-to-date on the back of stronger FX inflows from cocoa and gold exports. On a monthly basis, the CPI dipped by 0.4%, reversing the 0.9% rise seen in September.

The continued moderation in prices provides broad-based relief across the economy. For households, easing inflation improves real purchasing power. For firms, a more predictable price environment lowers input-cost volatility and allows businesses to plan production, investment, and inventory decisions with greater confidence. For the monetary policy authority, it enhances the case for additional monetary easing after the 650bps cut earlier in the year, as borrowing costs remain high relative to the new inflation path.

Looking ahead, inflation is expected to remain within the 6.0% to 10.0% target band, if exchange-rate stability is maintained and food supplies remain intact. However, risks persist from potential agricultural shocks, renewed currency volatility, or fiscal slippage as the election cycle approaches. Barring these pressures, the current disinflation path offers a firmer base for economic planning and supports a more stable macro outlook heading into 2026.

Domestic Events

Nigeria Plans Sale of State-Owned Refineries to Boost Efficiency and Cut Fuel Import Dependence

The Federal Government has indicated plans to sell or concession Nigeria’s four state-owned refineries (Port Harcourt, Warri, and Kaduna) as part of its ongoing downstream sector reforms. Despite their combined installed capacity of about 445,000 bpd, these refineries have operated far below potential for years, even after several rehabilitation attempts, including the USD1.48bn approved by the Federal Executive Council in 2021 for the Warri and Kaduna plants. The proposed divestment aims to attract private capital and technical expertise to revive the idle refineries, improve operational efficiency, and increase competition in the downstream petroleum segment following the removal of fuel subsidies. Through increased private participation, the government seeks to cut its fiscal burden from refinery maintenance and fuel imports, while advancing its broader agenda of market liberalization and transparency in the petroleum sector.

If implemented, the planned sale could transform Nigeria’s downstream oil market by reducing reliance on fuel imports, improving domestic supply stability, and conserving foreign exchange reserves. It also holds potential to ease fiscal pressures, support exchange rate stability, and moderate inflation through reduced imported fuel cost pass-through.

Nigeria’s Currency in Circulation Growth Slows, Reflecting Tighter Liquidity and Rising Digital Payment

According to the Central Bank of Nigeria, currency in circulation (the total amount of physical cash held by the public and used for transactions) grew by a mild 0.6% MoM to NGN4.96trn in September 2025, from NGN4.9trn in August. Despite this uptick, currency in circulation remains below the NGN5.05trn average recorded in the first half of the year. On a yearly basis, annual growth slowed to 14.9% in September, compared to 18.7% in August and 23.5% in July. This is also the slowest annual growth rate since December 2023, showing a continued moderation in cash usage.

The slower momentum comes amid tighter liquidity conditions the CBN has being taking to curtail inflationary pressures, such as the increased OMO auctions in recent months. Over the near term, currency in circulation growth is likely to stay mild as monetary conditions remain firm and digital payment adoption expands, helping to ease inflationary pressures by limiting excess cash in the system and reducing cash-driven demand. This trend should continue to channel more transactions through banks, fintechs, and mobile operators. However, if liquidity tightens too quickly, the possibility of temporary cash shortages cannot be ruled out, especially in rural and informal sectors where dependence on physical cash remains strong.

Nigeria Raises USD2.4bn Eurobond Amid Strong Investor Demand and Macro Confidence

Nigeria re-entered the international debt market with a USD2.4bn Eurobond issue, split across 10-year and 20-year maturities at coupons of 8.6% and 9.1%, respectively. The offering saw strong interest, with subscription exceeding USD13.0bn, a significant signal of investor confidence, especially given earlier concerns about investors’ sentiment after recent comments from the U.S. administration regarding Nigeria’s handling of religious tensions. The robust demand reflects improving market perception of Nigeria’s macroeconomic direction, helped by its addition to the watchlist for potential reclassification to the FTSE Russell Frontier Market Index and removal from the FATF greylist. While the pricing came at a slight premium, it remains broadly aligned with recent African issuances, such as Kenya’s 8.8% (12-year) and Angola’s 10.5% (10-year), reinforcing the view that investors are once again engaging African high-yield credits as global yields soften. Congo’s recent USD670.0mn issue after nearly two decades away further underscores that trend. The Proceeds from the bond will support the 2025 fiscal deficit and cover refinancing needs, particularly the USD1.1bn maturity falling Eurobonds due in November 2025. The inflow also provides a needed boost to external reserves, which should help stabilise the exchange rate in the short term. However, it does add to the country’s external debt load, at a time when debt service obligations are already sizeable -USD2.3bn as of H1:2025 , meaning fiscal pressures are unlikely to ease meaningfully without broader revenue and expenditure reforms.

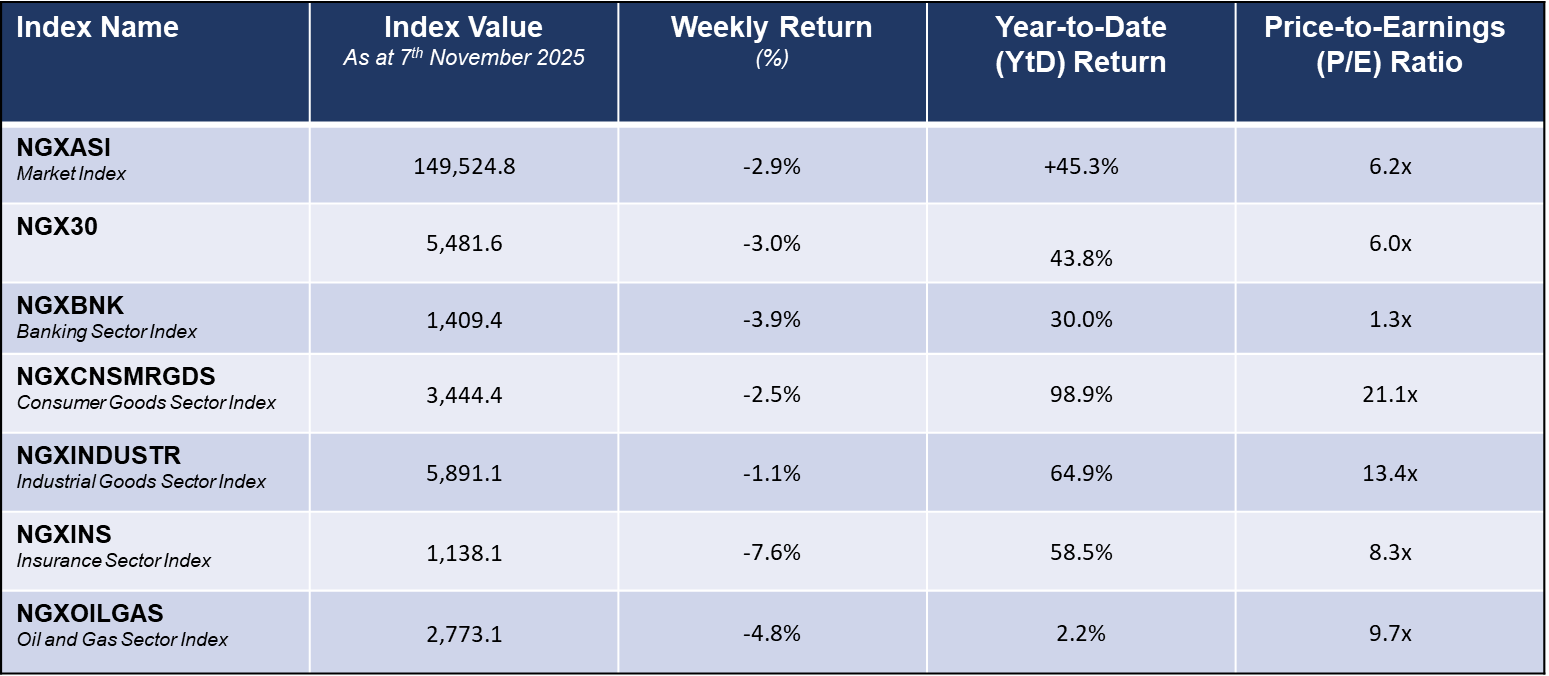

Equities Market – Sectorial Performance

Weekly Performance of Sectorial Indices

Fixed Income Market

In the Primary market, the Central Bank of Nigeria (CBN) held an OMO auction on Monday, offering NGN600bn across the 53-day and 81-day maturities. The auction saw strong investors’ demand with total subscriptions reaching NGN13trn, with demand mostly tilted towards the 81-day paper (NGN1.27trn). At the end of the auction, the CBN allotted NGN1.15trn across both tenors with stop rates at 21.6% and 21.8%, respectively.

Also, the CBN on behalf of the Debt Management Office (DMO) conducted its first Treasury Bills (T-bills) auction of the month on Wednesday, offering a total of NGN650.0bn across the three tenors. The offer ranged from NGN100.0bn in 91-day bill, NGN100.0bn in 182-day bill, and NGN450.0bn in 364-day bill. Investors’ demand was also significant with a total of NGN1.2trn, with demand majorly concentrated on the 364-day bill. At the end, the CBN allotted NGN546.2bn, at stop rates of 15.3%, 15.5% and 16.0% for the 91-day, 182-day and 364-day bills, respectively.

The FG returned to the Eurobond market with a USD2.4bn issuance which included a 10-year and 20-year tranche of (USD700.0mn and USD1.5bn, consecutively). Investors’ demand was strong with total bids exceeding USD12.7bn (excluding joint lead managers’ participation). At the end, the offered amount was raised across the 10-year (Jan-2036) and 20-year (Jan-2046) tenors, and yield were priced at 8.6% and 9.1%, respectively.

Activity in the T-bills secondary market signalled a bullish tone in anticipation of the primary auction in the week, as average yield inched down by 7bp to 17.4 from 17.5% in the previous week. The bullish momentum was driven by sustained demand for bills across all segments of the curve. However, demand was significant for the FEB-26 (-56bps), APR-26 (-32bps), and AUG-26 (-30bps and -29bps), resulting in notable yield compressions. Despite selloffs sentiment on the JAN-26 (+66bps) and JUL-26 (+33bps) papers, the market remained bullish.

In the bond market, the bullish momentum was also seen, with the average yield dipping by 13bps to 15.8% vs 15.9 in the previous week. Buying pressure dominated the short-end of the curve and was most pronounced on the JAN-16 (-40bps), MAR-24 (-39bps and -50bps), and JUL-14 (-44bps) papers. There were no selloffs in the week as activities were muted also at the longer-end of the curve, reflecting strong investors’ confidence despite fears associated President Trump’s genocidal statement. Meanwhile, the Eurobond secondary market was the reverse, entirely bullish, which was evident in the selloffs as average yield jumped to 8.0% from 7.7% in the previous week, a +31bps difference. The secondary market was significantly affected by President Donald Trump’s pronouncement of Nigeria as a country of particular concern. This impacted sentiments, despite Nigeria’s strong macro position. Notable selloffs were seen in NOV-18 (+116bps), NOV-17 (+45bps) and SEP-21 (+34bps).

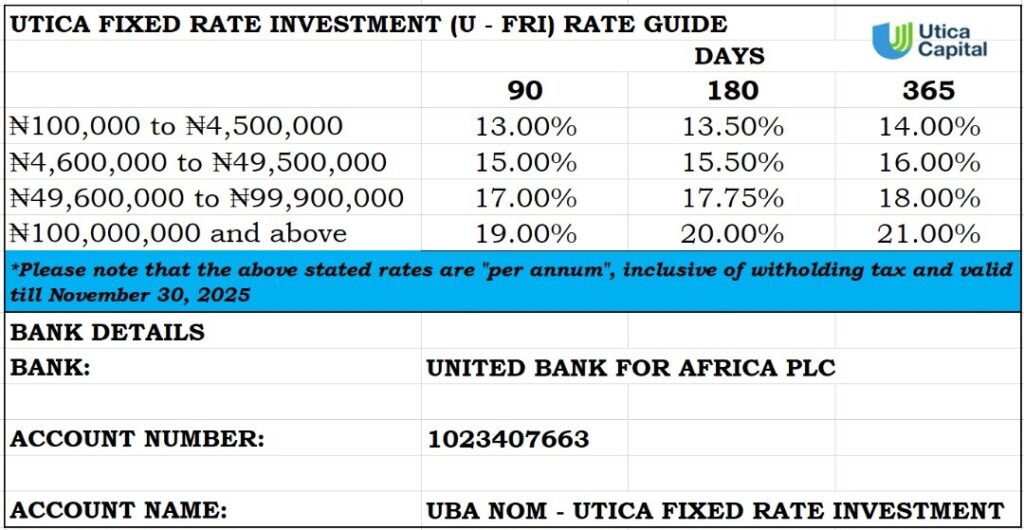

Fixed Income Opportunities for the week