World Bank Upgrades China’s 2025 Growth Forecast, Signals Slower Momentum Ahead

Global Macro Highlights

World Bank Upgrades China’s 2025 Growth Forecast, Signals Slower Momentum Ahead

The World Bank has raised its 2025 GDP growth forecast for China to 4.8%, up from its earlier estimate of 4.0%, despite ongoing trade tensions with the U.S. This upward revision is driven by stronger export performance, targeted government stimulus, and resilience in domestic sectors. China’s growth has been supported by increased shipments to Southeast Asia and Europe, which have offset weakness in U.S. markets, as well as stimulus aimed at bolstering consumption. The World Bank also cautioned that growth may decelerate to 4.2% in 2026, citing weakening export demand and the need to gradually reduce stimulus to rein in debt pressures. Supporting the positive growth outlook is the increase in the country’s manufacturing PMI to 49.8pts in September from 49.4pts in August indicating a recovery from April’s sharp decline, further supporting the better growth outlook for 2025. However, since much of the government stimulus has been debt-financed, the need to gradually reduce fiscal support amid rising public debt levels could dampen spending, thereby aligning with World Bank’s expectation of slower growth in 2026. Additionally, the lingering real estate crisis is expected to further weigh on economic activity, adding to downside pressures on growth outlook. Overall, this upward revision of 2025 outlook signals improving short-term economic performance as growth is expected to moderate in 2026 as export demand weaken. Looking ahead, the potential slowdown in China’s growth rate by 2026 signals possible decline in global demand, particularly for oil and agricultural commodities. Such development could keep oil prices at their current low levels, posing downside risks to Nigeria’s FX inflows, external reserves and potentially tightening the country’s external liquidity position.

World Bank Lifts Sub-Saharan Africa’s 2025 Growth Forecast to 3.8%, Citing Stronger Stability and Recovery

Similarly, the World Bank raised its 2025 GDP growth forecast for Sub-Saharan Africa upward to 3.8% (vs. 3.5% previously), hinged on the region’s progress in price stability and economic recovery. The institution noted lower inflation, stronger agricultural output, and improved fiscal discipline in key economies such as Nigeria, Ethiopia, and Côte d’Ivoire, alongside a more stable FX environment and recovering foreign investment across the region. We believe this upward review is an indication of rising optimism towards Sub-Saharan Africa and is likely to encourage foreign exchange inflows and increased portfolio and foreign direct investment inflows. Nonetheless, lingering challenges, including high debt levels, structural unemployment, and climate-related vulnerabilities, could temper gains if not addressed. Essentially, we expect the region’s growth momentum to accelerate moderately, provided that governments maintain fiscal prudence, macroeconomic stability, and policy reforms that support private sector expansion. In addition, we believe it is pertinent that Sub-Saharan Africa fiscal leaders sustain efforts to reduce debt vulnerabilities and diversify export bases to sustain long-term growth.

Kenya’s Central Bank Cuts Interest Rate to 9.3% to Boost Lending and Growth Amid Stable Inflation

During the week, the Central Bank of Kenya (CBK) lowered its benchmark interest rate for the eighth consecutive time, to 9.3% (down 25bps from 9.5%) to stimulate private sector lending and boost economic growth. In our view, the dovish tone of the Kenyan monetary authority mirrors continued confidence in price stability (inflation at 4.6% in September, comfortably within the bank’s 2.5% – 7.5% target range). According to the Monetary Policy Committee (MPC), the 25bps reduction is aimed at expanding credit and sustaining business activity while keeping inflation expectations anchored. The CBK also raised its 2026 GDP growth forecast to 5.5% (from 5.4%), citing the resilience of services, agriculture, and industrial recovery, while maintaining its 2025 outlook at 5.2%. The CBK rate cut is expected to put an upward pressure on inflation in the near term as lower cost of borrowing may increase credit access and demand. This dovish stance is also expected to support the equities market through positive investor sentiment and liquidity. In contrast, the fixed income market may turn bearish, as lower yield make these securities less attractive, potentially triggering capital outflows as investors seek higher-yielding assets. Looking ahead, we expect the CBK to maintain its dovish stance, prioritizing growth and credit availability given that inflation remains within its target range.

Angola Re-enters Eurobond Market with USD1.5bn Dual-Tranche Issuance to Strengthen Fiscal Position and Investor Confidence

Angola made a re-entry into the international capital markets, for the first time since 2022, as it issues a dual-tranche USD1.5bn on the back of relatively stronger fiscal strength and improved investor sentiment. The government issued five-year and ten-year maturities, priced at 9.8% and 10.5%, respectively, to partly refinance bonds maturing in November 2025 and support its USD14.9bn 2025 financing plan. In the immediate term, the Eurobond issuance enhances Angola’s fiscal flexibility and external liquidity, enabling it to meet debt obligations and reduce rollover pressures. However, public debt, currently estimated at c.USD58bn, will increase due to the new issuance. Although this is a welcome initiative, Angola might be exposed to external vulnerabilities, particularly fluctuations in oil prices and global financing conditions. Overall, the bond issuance is expected to strengthen Angola’s short-term fiscal and external positions and reinvigorate investor confidence in the market. The additional funding also provides the government with the fiscal space to sustain critical spending on infrastructure and social programs, potentially supporting a further recovery in economic growth from the current 4.4% level.

Domestic Events

Nigeria’s PMI Climbs to 54.0pts in September, Signaling Stronger Economic Expansion Across Key Sectors

The Central Bank of Nigeria announced that the composite PMI increased to 54.0pts in September from 51.7pts in August, (10th consecutive month of growth). The expansion in economic activity was broad based as expansion was recoded in all major sectorial indices including Industry, Services, and Agriculture, and key components such as output, new orders, employment, and supplier delivery times showed improvement. By sectors, the Industry PMI rebounded to 51.4pts (from 49.1pts in August 2025) as 11 subsectors out of 17 expanded, led by printing and related support activities. The Services PMI expanded to 54.7pts, marking its eight consecutive expansion, while the Agriculture Sector PMI rose to 54.8 pts (vs 53.9pts previously), its fourteen consecutive month of expansion driven by growth across all subsectors, with Forestry posting the strongest growth. This is owing to increased business confidence, stronger demand, and better supply chain functioning, supported by a more stable macroeconomic environment. This sustained growth in the PMI suggests a positive outlook for Q3 GDP performance, indicating continued recovery in non-oil output and contribution to growth. We expect the PMI to maintain its expansionary trend in the near term, supported by improving macroeconomic environment and easing cost pressures. However, risks of FX volatility, and infrastructure constraints could drag growth.

FG Plans USD2.8bn External Borrowing, Including Debut USD500mn Sovereign Sukuk, to Refinance Debt and Support 2025 Budget

The Federal Government of Nigeria has unveiled plans to raise USD2.8bn from external sources, including a USD500mn debut sovereign sukuk (its first foray into the global Islamic finance space), as part of efforts to refinance maturing Eurobonds and bridge the 2025 fiscal deficit. The proposal, sent to the National Assembly, also seeks approval for USD2.3bn in new foreign loans to support budgetary and infrastructure financing needs. We believe that these efforts is a strategic approach to managing Nigeria’s debt profile which is currently at NGN149.4trn, supporting economic needs, and keeping investor confidence amid fiscal pressures Looking ahead, we note this proposal once approved, could further increase Nigeria’s external and total debt stock, currently at USD46.0bn and NGN149.4trn, respectively, thereby increasing debt servicing obligations. Nonetheless, we expect the planned issuance to attract investors interest, supported by improving market sentiment and recent sovereign rating upgrades such as Fitch’s upgrade to B and Moody’s to B3 in 2025. Additionally, a well-executed return to the international market could bolster external reserves, strengthen investor confidence, and ease near-term refinancing pressures.

FTSE Russell Places Nigeria on Watch List for Possible Return to Frontier Market Status, Signaling Renewed Investor Confidence

During the week, global index provider FTSE Russell placed Nigeria on its watch list for potential reclassification from unclassified to Frontier Market status, citing improvements in foreign exchange (FX) liquidity and repatriation processes. Before now, Nigeria was removed from the FTSE Frontier Market Index in September 2023 after persistent FX access challenges and capital return delays which hindered investors’ ability to exit the market. The exclusion, which followed similar actions by other global index providers including MSCI and S&P Dow Jones, significantly reduced Nigeria’s visibility among foreign portfolio investors and limited passive capital inflows. Hence, we believe this review signals renewed investor attention toward Nigeria’s capital market reforms and policy direction. Also, potential reclassification could enhance the country’s visibility among global fund managers and attract passive inflows from investors tracking FTSE Frontier indices, thereby improving market liquidity and foreign participation on the Nigerian Exchange (NGX). Looking ahead, Nigeria’s full reinstatement into the FTSE Frontier Market category could unlock sizable passive inflows from global funds tracking FTSE indices, strengthening foreign participation and boosting liquidity in the Nigerian Exchange (NGX). Nevertheless, the sustainability of FX reforms, predictable capital repatriation, and consistent policy implementation remain critical for reclassification in the next review cycle.

Fixed-Income Market

• The CBN held a Treasury Bills auction on 8th October 2025, offering NGN570.0bn across 91, 182 and 364-day maturities. Total subscriptions stood at NGN1.1trn, with demand strongest for the 364-day paper (NGN986.3bn vs. NGN350.0bn offered). The CBN allotted NGN25.4bn on the 91-day at 15.0%, NGN41.3bn on the 182-day at 15.3%, and NGN503.3bn on the 364-day at 15.8%.

• The secondary bonds market traded bullish, with buying interest concentrated at the short and long-end of the curve, notably in JAN-26 (- 83bps), MAR-27 (-71bps), and MAR-35 (-50bps). In contrast, a sell-off was observed in MAY-33 (+14bps). Overall, the average bond yield declined by 29bps to 16.0%.

• Similarly, the secondary T-bills market closed on a bullish note, as strong demand across all tenors pushed average yields down by 54bps to 17.4%. The most notable declines were concentrated along the mid-end of the curve particularly in the APR-26 (-94bps), MAY-26 (- 83bps), and JUL-26 (-72bps).

• On the other hand, the Eurobond market closed the week on a bearish note as average yield increased to 8.1%, up from 7.9% in the prior week. Sell-offs was seen across all curve, particularly the MAR-29, FEB-30, and FEB-32 which recorded yield increases of 49bps, 33bps and 25bps, respectively. In contrast, buying interest was observed in the NOV-25 which recorded a yield decline of 49bps to 6.7%.

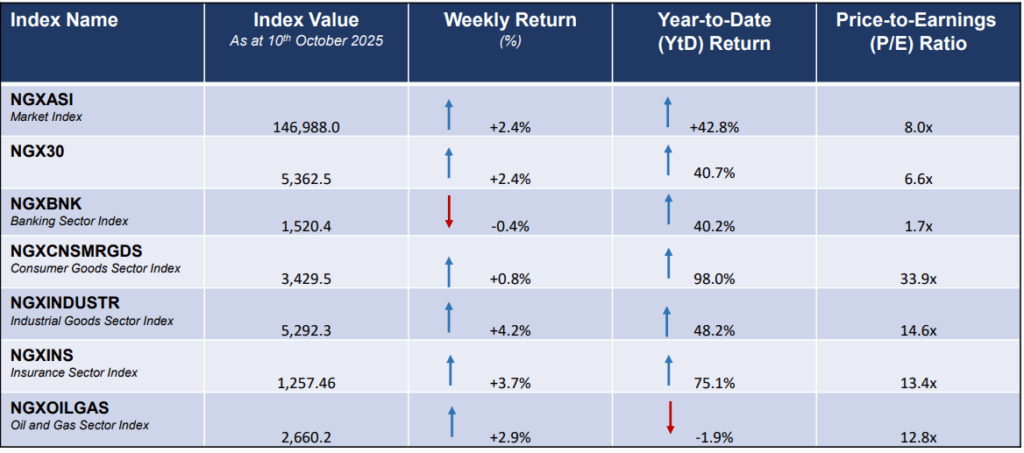

Equities Market – Sectorial Performance

Weekly Performance of Sectorial Indices

Market Snapshot

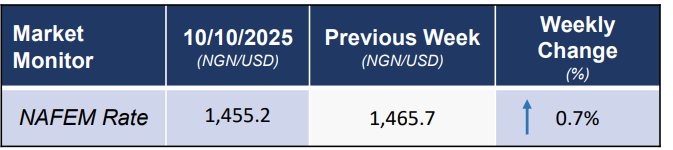

FX Monitor

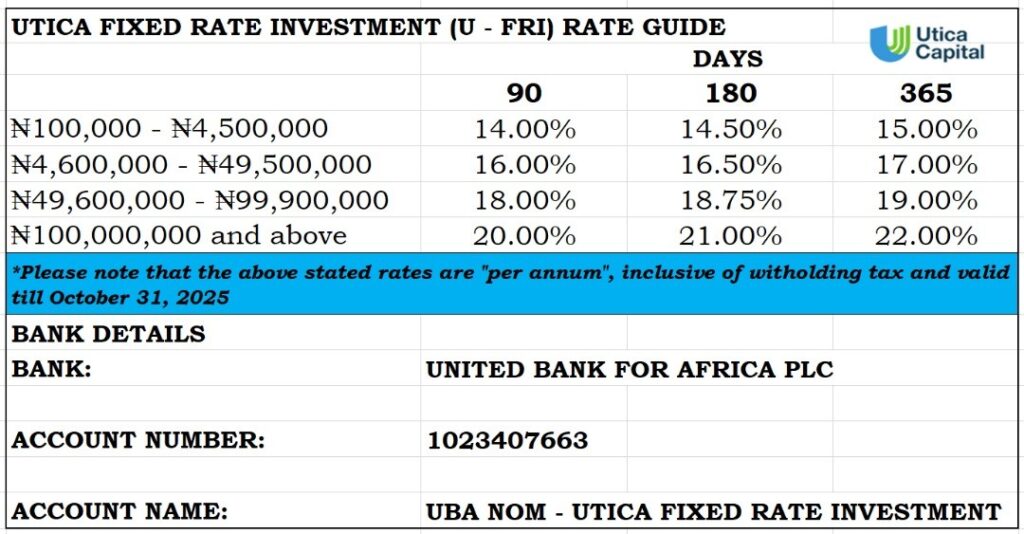

Fixed Income Opportunities for the week