CBN Holds MPR at 27% as MPC Signals Confidence in Economic Stability

Global Macro Highlights

UK Autumn Budget Tightens Taxes on Property, Dividends and Savings

According to the UK Office for Budget Responsibility, the Autumn Budget introduced a series of tax measures aimed at boosting revenue and encouraging investment through regulated channels. The government is raising taxes on property, dividend and savings income, reflecting the fact that income from those sources faces no equivalent of National Insurance that employees pay. These measures signal tighter personal tax conditions, meaning higher tax liabilities for company directors who receive dividends, landowners earning property income, and investors holding assets outside ISAs or pensions. Investors and asset owners holding shares or property outside tax-efficient wrappers, such as ISAs or pension accounts, will experience lower post-tax returns.

Looking ahead, households and small investors are likely to face tighter disposable incomes and slimmer after-tax returns, which could dampen consumer spending and investment risk appetite. Businesses, particularly smaller firms or owner-managed companies, may feel pressure on long-term planning and ownership transitions. At the macro level, the changes point to higher taxes on passive income, which may slow wealth accumulation, but the push toward ISAs, pensions and equity investment is intended to redirect savings into more productive areas, potentially providing a modest boost to capital-market activity over time.

U.S. Lifts 15% Tariff on Ghanaian Cocoa and Key Agricultural Exports

Ghana’s government has confirmed that the United States has removed the 15.0% tariff previously applied to Ghanaian cocoa and other key agricultural exports, including cashew nuts, avocados, bananas, mangoes, and oranges. The move is expected to ease trade conditions for Ghanaian exporters, which accounted for about 17.6% of Ghana’s cocoa shipments in 2024.

The tariff removal reduces market-entry costs, enhances price competitiveness, and is likely to expand profit margins, particularly for cocoa producers. Also, earnings from Stronger demand are expected to boost foreign-exchange inflows and stimulate growth across the country’s agricultural value chain. In the U.S., food and chocolate manufacturers stand to benefit from lower raw material costs, helping ease production expenses amid elevated input inflation and potentially moderating consumer-price pressures on these products.

Looking ahead, the policy is expected to deliver significant benefits for Ghana, especially in cocoa, where around 78,000 metric tons are exported to the U.S. annually, while also supporting profitability across other agricultural exports. For the U.S., it reinforces stronger margins for food and chocolate manufacturers while strengthening bilateral trade ties.

Bank of Ghana Cuts Policy Rate to 18% as Disinflation Deepens

The Bank of Ghana (BoG) cut its benchmark policy rate by 350 basis points to 18.0%, marking the third consecutive reduction this year and a cumulative 1,000 basis points cut in 2025. This decision follows a sharp deceleration in inflation, which fell from 23.5% YoY in January 2025 to 9.4% in September, and further to 8.0% in October, comfortably within the BoG’s 6%–10% target range.

The central bank has also returned to using the 14-day Treasury bill as its primary open-market instrument, signaling a renewed focus on short-term liquidity management. The policy rate reduction is expected to lower borrowing costs for businesses and households, stimulate credit growth, and encourage investment and consumption across the economy. Reduced financing costs should also ease debt-servicing pressures for both the public and private sectors, supporting overall fiscal and financial stability.

Looking ahead, we expect the Bank of Ghana to maintain this easing cycle, supported by moderating inflation and a stable macroeconomic conditions. Lower borrowing costs are also likely to stimulate stronger growth in the real economy, creating opportunity for sustained private-sector expansion.

World Bank Lifts Kenya’s 2025 Growth Outlook Amid Construction Rebound

The World Bank has revised Kenya’s 2025 growth forecast upward to 4.9% (from 4.5% previously), reflecting improved confidence in the country’s economic momentum, particularly within the construction sector, which accounts for 6.4% of GDP. Kenya’s economy expanded by 5.0% in Q2 2025 (vs. 4.6% in Q2 2024), extending the 4.9% growth recorded in Q1. This performance was underpinned by moderate gains in agriculture, forestry and fishing (4.4% vs. 4.9% in Q2 2024), alongside stronger recoveries in transportation and storage (5.4% vs. 3.8%) and financial and insurance activities (6.6% vs. 5.1%). A major factor behind the improved outlook was the strong rebound in construction, which grew 5.7% (up from 3.0%). Looking ahead, Kenya’s growth trajectory is expected to strengthen further over the medium term, driven by broad-based sectoral gains and the ongoing recovery in construction and services. Softer inflation, easing domestic borrowing costs, and a more stable interest-rate environment should bolster consumption and investment, paving the way for a stronger and more sustainable expansion. Overall, improving macroeconomic conditions suggests that Kenya is well positioned to consolidate recent growth gains as policy stability and sectoral activity continue to improve.

Global Equities Market

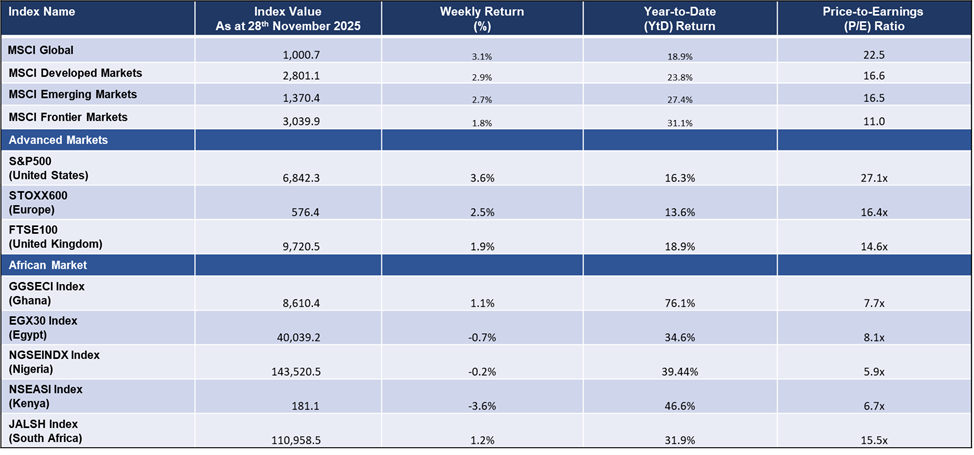

Weekly Performance of Major Global Indices

Domestic Events

CBN Holds MPR at 27% as MPC Signals Confidence in Economic Stability

At its 303rd MPC meeting, the Committee voted to keep the Monetary Policy Rate (MPR) unchanged at 27.0%. Other major policy parameters were also retained: the Cash Reserve Ratio (CRR) at 45.0% for Deposit Money Banks, 16.0% for Merchant Banks, and 75.0% for non-TSA public sector deposits and Liquidity Ratio held at 30.0%. However, the asymmetric corridor was adjusted to +50bps/–450bps around the MPR (from +250bps/–250bps previously). The overall decision reflects the Committee’s confidence in current macroeconomic momentum, underpinned by a sustained disinflation trend, a stable foreign exchange market, and higher external reserve buffers.

The corridor adjustment is expected to incentivise banks to extend more credit to the real sector, as the lower Standing Deposit Facility (SDF) rate reduces the appeal of keeping idle liquidity with the CBN.

Looking ahead, maintaining the policy rate is expected to consolidate earlier monetary gains and support inflation moderation toward the 15.00% short-term target, while preserving exchange rate stability and strengthening domestic economic activity. For the financial market, we expect yields to continue trending downward in the fixed income space, reinforcing the prevailing bullish sentiment. Meanwhile, in the equities market, mixed sentiment is likely to persist.

Nigeria’s PMI Hits 2025 High, Marking 12 Consecutive Months of Expansion

According to the Central Bank of Nigeria (CBN) Purchasing Managers’ Index (PMI), shows that Nigeria’s economy expanded for the twelfth consecutive month in November 2025, with the PMI rising to 56.4 points from 55.4 points in October, a +1.8% MoM increase and the highest reading this year. The growth was broad-based, led by the agriculture at 58.2 points, Services at 56.8 points, and Industry at 54.2 points. Out of the 36 subsectors, 29 recorded expansions, with water supply, sewerage and waste management (65.6 points), transportation equipment (65.3 points) and Forestry (64.6 points) leading the gains, while only 7 subsectors contracted (an improvement from 11 in October), with paper products reporting the highest decline at 42.5 points. This performance underscores stronger manufacturing output, steady business activity, resilient demand and favourable agricultural conditions. Looking ahead, we expect sectoral expansion to persist, supported by improving macroeconomic fundamentals majorly from moderating inflation and a more stable exchange-rate. The recent policy corridor adjustment is expected to encourage banks to extend more credit to the real sector, sustaining growth momentum across industries.

Equities Market – Sectorial Performance

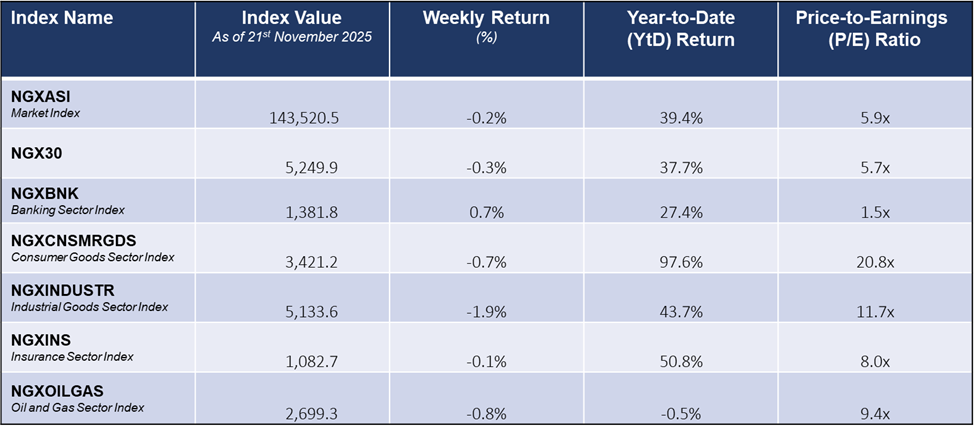

Weekly Performance of Sectorial Indices

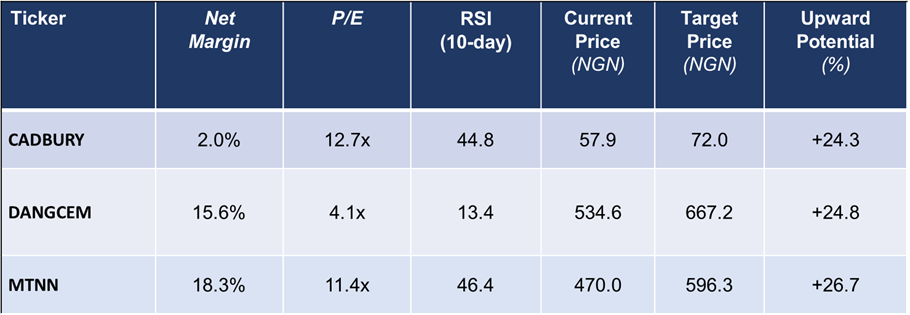

Stock Top Picks for The Week

Fixed Income Market

Fixed Income Opportunities for the week