FGN Imposes 15% Import Duty on Refined Fuel to Boost Local Refining and Ease FX Pressure

Global Macro Highlights

Fed Cuts Rates Again, Ends Quantitative Tightening to Support Growth Amid Rising Unemployment

The Federal Reserve lowered its benchmark interest rate by 25bps to a range of 3.8%–4.0% at its October 2025 FOMC meeting, marking its second consecutive rate cut this year. The decision comes despite the elevated inflation rate which still stands above the bank’s 2% target, as the Fed maintained a dovish stance to control the US rising unemployment levels. In a separate decision, the Fed moved to end quantitative tightening policy which has been on since 2022, to stabilize liquidity levels in the US economy in addition to the dovish stance.

The rate cut is expected to ease borrowing costs, thereby improving access to credit for households and businesses and potentially boosting investment and productivity growth. However, lower interest rates could also drag yields downward in the fixed income market prompting investors to shift towards equities or higher-yielding market such as emerging markets. This could result in a bullish momentum in the fixed income markets in emerging economies.

Looking ahead, the Fed might adopt a hold stance, given limited data availability following the government shutdown. We expect the combination of the dovish stance and end of quantitative tightening to support economic activity and output in the short-term however, a stronger consumption could inflict upward pressure on inflation. Meanwhile, declining Treasury yields could trigger sell-offs in the dollar, leading to a slight depreciation in the near term.

U.S. and China Reach One-Year Trade Deal, Easing Tariffs and Supply Chain Pressures Across Key Industries

The US and China has reached a trade deal during the week. Under this agreement, the US dropped the proposed 100% tariff on Chinese goods and reduced fentanyl-related tariff from 20% to 10%, bringing the total tariff on China down to 47% from the 57% previously. In return, China agreed to pause the export controls on rare earth elements announced in October for a year, they also agreed to purchase significant amount of soybean from the US and tighten control of illicit fentanyl trade.

Following announcement of this deal, global oil prices eased as Brent crude and WTI dropped slightly pricing in the fact that the deal, which spans for a year, could be a short-term de-escalation of the trade dispute. Nevertheless, this deal may help ease supply chain constraints around rare earth elements, a key input for high tech and manufacturing industries, thereby alleviating cost pressures for US producers. In addition, reduced tariff on fentanyl which is highly essential for pain management and anesthesia in the US healthcare industry, could soften cost pressures for healthcare manufacturers while the pause on export controls on fentanyl for one year could also ease uncertainty, improve trade sentiment, and support global trade stability.

We expect easing cost pressures in the automobiles, electronics, and technology; particularly industries which are heavily reliant on rare earth materials. The country’s healthcare sector could also see some cost relief following the decline on fentanyl-related input costs. Overall, these could contribute to a modest downward pressure on US inflation while providing a moderate boost to Chinese manufacturing activities.

ECB Holds Rates Steady at 2.0% to Support Growth as Inflation Nears Target

The European Central Bank (ECB) kept its deposit facility rates unchanged at 2.0% for the third consecutive time. This direction was due to the fact that inflation was near its medium-term target and a modest rebound in the eurozone economy. Inflation had edged up to 2.2% YoY in September, from 2.0% YoY in August, but the ECB noted its assessment of the outlook was “broadly unchanged”, and the economy grew by 0.2% QoQ in Q3:2025, slightly higher than the previous month.

We expect that this dovish stance is likely to maintain stable borrowing cost and this could boost lending and investments by both businesses and household thereby supporting the broader economic growth. However, the implication for financial markets may be mixed. While equity markets may benefit from improved liquidity and stronger earnings sentiment, fixed-income yields could face downward pressure, reducing returns for conservative investors. In addition, a prolonged rate hold could exert mild depreciation pressure on the euro, particularly if the U.S. Federal Reserve maintains a comparatively tighter policy stance.

Eurozone Growth Slows to 1.3% as Southern Economies Drive Expansion Amid Weak Industrial Output

The Eurozone grew by 1.3% YoY in the third quarter of 2025, tapering from 1.5% recorded in Q2:2025, indicating a continued slowdown in the region’s recovery. The expansion was led by growth in southern economies such as Spain (+2.8% vs 3.1%), Portugal (+1.6% vs 1.7%), and France (0.9% up from 0.7%) driven by tourism and services demand. However, industrial-heavy economies, like Italy and Germany remained steady at 0.4%YoY and 0.3%YoY respectively reflecting subdued growth amid sluggish global demand and weak factory output. On a quarterly basis, Eurozone GDP rose 0.2% QoQ, an improvement from the 0.1% growth recorded in the previous quarter.

The soft growth momentum reflects the persistent structural challenge, muted productivity, weak investment appetite, and subdued global demand driven by the tariff driven trade war. With inflation which is currently at 2.1% gradually aligning to the European Central Bank’s (ECB) 2% target, the monetary authority might maintain a hold stance, prioritising growth support while monitoring inflationary pressures.

Looking ahead, growth in the region is likely to remain modest as easing inflation could bolster household spending and domestic demand. Additionally, the dovish monetary policy stance could help support business investments while sustained strong tourism activity, could remain a key growth driver. Furthermore, easing global trade tension following the recent trade agreement between the US and China, under which the U.S. cut tariffs on Chinese imports to 47% (from 57%) and China paused export controls on rare earth materials, could ease global concerns and uncertainties thereby reviving global demand and supporting the Eurozone industrial sector and output.

Domestic Events

FIRS Reinstates 10% Withholding Tax on Short-Term Securities to Boost Non-Oil Revenue

The Federal Inland Revenue Service (FIRS) has issued a new directive instructing banks, stockbrokers, and other financial institutions to immediately implement the 10% withholding tax (WHT) on interest earned from short-term securities such as Treasury bills, promissory notes, and bills of exchange. The tax will be deducted at source.

This marks the reinstatement of a policy that had been suspended since January 2012 to deepen the local debt market and attract investor participation. Its revival aligns with the government’s broader goal of increasing revenue from non-oil sources and narrowing the fiscal deficit.

However, the move is expected to reduce after-tax yields on Treasury bills, prompting investors to demand higher rates at the primary auction. Consequently, interest rates on commercial papers and corporate bonds may rise, given that treasury bills yields often serve benchmark for other short-term debt instruments. Additionally, the reinstated tax could shift investor preference toward tax-exempt government bonds or equities, particularly if relative returns appear more appealing.

Looking ahead, we expect demand for short-term securities to soften, while secondary market yields may face mild downward pressure as investors reprice for the tax impact. Overall, market participants are likely to adopt a more comparative approach, weighing the net returns on Nigerian short-term instruments against those in other emerging markets.

FGN Imposes 15% Import Duty on Refined Fuel to Boost Local Refining and Ease FX Pressure

In a separate update, the FGN has approved a 15% import duty on refined petrol and diesel, marking a significant shift in downstream oil and gas sector. The decision comes as part of broader efforts to strengthen Nigeria’s refining capacity, stabilize the downstream market, and reduce dependence on imported petroleum products. With the 650,000bpd Dangote Refinery now operational, alongside other modular refineries, the government’s goal is to create a more sustainable, self-sufficient energy system.

The levy, applied on the cost, insurance, and freight (CIF) value of imported fuel, could raise landing costs thereby making imports less competitive relative to locally refined products. While the policy supports local refiners such as Dangote and modular domestic plants by improving their price competitiveness, it could trigger short-term inflationary pressures as higher landing costs feed into pump prices, transport costs, and food prices. On the fiscal side, the duty is expected to generate additional non-oil revenue and reduce FX outflows tied to fuel imports offering more support to the exchange rate market.

We anticipate that this policy could strengthen the market share for locally refined products, positively influence prices, and reduce import dependence thereby easing pressure on the Naira. However, we note that any disruption in domestic supply—whether from refinery maintenance or feedstock shortages, could exert upward pressure on inflation.

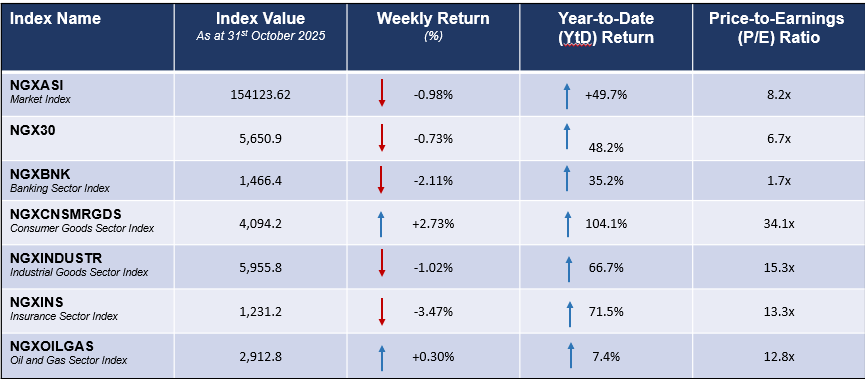

Equities Market – Sectorial Performance

Weekly Performance of Sectorial Indices

Fixed Income Market

The Debt Management Office (DMO) conducted the FGN bond auction during the week, offering a total of NGN260.0bn across the AUG-30 and JUN-32 instruments. Total subscriptions declined by 15.9% to NGN1.1trn, while total allotments dropped by 45.6% to NGN313.8bn. Resultantly, stop rates on the AUG-30 and JUN-32 bonds moderated by 17bps and 35bps to 15.8% and 15.9%, respectively (vs 16.0% and 16.2% previously).

Activity in the T-bills secondary market was relatively quiet, closing marginally bullish as the average yield inched down by 1bp to 17.5%. The mild bullish momentum was driven by sustained demand for short-to-mid-tenor bills, resulting in notable yield compressions on the DEC-25 (-6bps), MAR-26 (-16bps), and MAY-26 (-9bps) maturities. Conversely, the long end of the curve witnessed renewed selling pressure, particularly on the SEPT-26 (+62bps) and OCT-26 (+44bps) papers, as investors repositioned ahead of upcoming primary auctions.

In the bond market, the bullish momentum reversed, with the average yield rising by 3bps to 15.9%. Selling pressure dominated across the curve, most pronounced on the JAN-26 (+37bps), APR-29 (+33bps), and JUN-33 (+42bps) papers. Nonetheless, selective buying interest was observed on the JAN-35 (-58bps), FEB-31 (-22bps), and APR-29 (-15bps) maturities, reflecting investors’ preference for longer-duration assets amid expectations of stable near-term rates.

Meanwhile, the Eurobond market extended its bullish momentum, closing the week on a strong note as the average yield declined by 15bps to 7.7% (from 7.8% previously). The rally was broad-based across maturities, with notable yield compressions on the FEB-30 (-19bps), NOV-47 (-17bps), and NOV-25 (-15bps) instruments, supported by renewed risk appetite following the U.S. Fed’s rate cut.

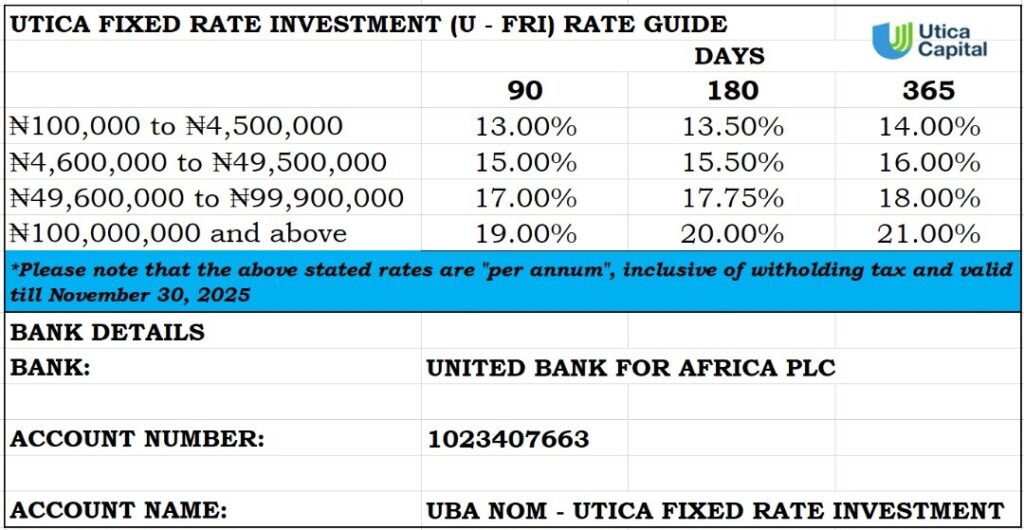

Fixed Income Opportunities for the week