Nigeria Launches Digital Treasury Platform to Curb Revenue Leakages and Boost Transparency

Global Macro Highlights

U.S. Inflation Edges Higher in September Amid Energy Price Surge, Core Measures Ease

The Consumer Price Index (CPI), as reported by the U.S. Bureau of Labor Statistics (BLS), registered a 3.0 YoY increase in September 2025, a slight acceleration from the 2.9% YoY rise observed in August. On a month-over-month (MoM) basis, the CPI advanced by 0.3%. This increase was primarily driven by a significant 4.1% MoM surge in gasoline prices, which offset declines in both food prices and shelter costs.

In contrast, Core CPI, which excludes the more volatile food and energy components, showed deceleration to 3.0% YoY in September from 3.1% in August. A key factor in this moderation was the shelter index, which accounts for over one-third of the total CPI basket. This index grew by only 0.1% MoM—its smallest monthly increase since 2021. Furthermore, food inflation remained subdued, supported by declining prices for grains and meat. However, modest price increases were noted in apparel and household furnishings, likely reflecting the pass-through of costs from tariff-related impacts on imported goods. Despite the moderation in Core CPI, headline inflation continues to exceed the Federal Reserve’s 2.0% target, primarily due to energy price volatility and tariff effects.

Disinflation is expected to continue in core measures driven by softening shelter costs and subdued demand, though an uptick in headline figures could emerge from volatile energy prices and escalating tariff pass-throughs on imported goods like apparel. However, we expect the Fed to likely deliver a rate cut to prioritize labor market risks over lingering price pressures.

U.S. Sanctions on Russian Oil Giants Tighten Global Supply, Drive Up Crude Prices

The U.S. Department of the Treasury imposed restrictive sanctions on Rosneft and Lukoil, Russia’s two largest oil producers. These measures include freezing U.S. assets and restricting dollar transactions, effectively isolating the firms from major Western financing and trade infrastructure. This action directly targets Russia’s fiscal stability, as oil and gas exports account for over one-third of the nation’s federal budget revenue.

Following the announcement, Brent crude prices immediately rose by 4.6% as market participants priced in potential disruptions to Russian export volumes. This anticipated contraction in near-term supply is expected to tighten the global oil balance. While Russia will attempt to reroute volumes to non-Western markets, structural limitations in logistics, insurance, and financing might cap the full replacement of lost Western demand.

The U.S. sanctions will likely disrupt Russia’s oil exports, forcing buyers in India and China to seek costlier alternatives and keeping global oil supply tight, which could put upward pressure on crude prices. This tighter market could benefit U.S. and allied oil producers with higher revenues, but it poses a clear risk of higher energy costs fueling inflation and slowing economic growth in major importing nations.

China’s Growth Slows to 4.8% in Q3 2025 Amid Weak Domestic Demand and Rising Trade Tensions

China’s economy expanded by 4.8% YoY in Q3 2025, slowing from 5.2% in the previous quarter and marking the weakest growth in a year. Quarterly GDP rose 1.1% QoQ, keeping the economy broadly aligned with its 5.0% annual growth target despite the loss of momentum.

Industrial production provided the primary support, rising 6.5% YoY. This acceleration was largely driven by robust external demand for high-value manufactured goods, including machinery and electronics. This resilience reflects the successful shift of policy support toward strategic advanced manufacturing sectors, which have captured global market share.

However, this export-led relief is likely temporary, as growth risks increase from sustained global trade tensions and the fading of any short-term “front-loading” effects by global buyers anticipating future tariffs. Conversely, domestic consumption remains the primary drag. Retail sales grew just 3.0% YoY in September, signaling persistently subdued household demand. Consumer caution stems from sluggish income growth and deep-seated structural weakness in the property and labor markets.

China’s economy is generally expected to continue its slowdown till the end of the year, driven primarily by persistent weakness in the property sector and rising external risks like increasing US tariffs, which offset the positive impact of policy support and strong momentum in high-tech manufacturing and exports.

UK Inflation Holds Steady at 3.8% as Price Pressures Ease

The UK’s headline inflation held steady at 3.8% YoY in September 2025, matching August’s pace and defying expectations of a rise by the Bank of England(BOE). The stability came as lower airfares, cheaper entertainment, and softer food prices offset higher transport and fuel costs. Core CPI eased slightly to 3.5% from 3.6%, while services inflation stayed firm at 4.7%.

This trend reflects a gradual normalization in price growth as supply-side pressures ease and consumer demand weakens. The decline in food and entertainment prices suggests households are becoming more cautious with discretionary spending. However, energy-related transport costs continue to pose risks, signaling that the inflation path remains uneven and vulnerable to global price shocks.

Inflation is expected to continue easing in the near term, as softer household spending and a cooling labor market reduce price pressures. However, with services inflation and wage growth still firm, the pace of disinflation will likely be gradual rather than sharp. This means inflation may not return to the Bank of England’s 2% target in the near term. Given this outlook, the BoE is likely to keep interest rates on hold for now to ensure inflation continues to slow sustainably. If the downward trend proves consistent and underlying pressures ease further, the Bank could start cutting rates cautiously in the medium term to support growth without undermining price stability.

Domestic Events

Nigeria Launches Digital Treasury Platform to Curb Revenue Leakages and Boost Transparency

The Federal Ministry of Finance has launched the Federal Treasury Receipt (FTR) platform a digital payment verification system aimed at curbing revenue leakages and improving transparency across Ministries, Departments, and Agencies (MDAs). The initiative is part of the broader Revenue Optimization and Assurance Programme, alongside the Central Billing System (CBS) and the Revenue Optimization and Assurance Platform (RevOp), both introduced earlier in August 2025.

The FTR enables every payment to the federal government to be traceable, verifiable, and reconciled in real time, addressing issues of unremitted funds, double billing, and weak audit trails. The pilot phase currently covers ten MDAs over a 30-day testing period before nationwide rollout.

This reform is fiscally significant, aligning with the government’s objective to boost non-oil revenue, strengthen public financial management, and minimize fiscal leakages that have historically widened Nigeria’s budget deficit.

In the near term, the fiscal gains will depend on the speed of adoption and system integration across MDAs. However, if effectively implemented, the FTR could deliver a structural improvement in Nigeria’s revenue management framework, enhancing fiscal resilience and supporting macroeconomic stability into 2026. Improved transparency and discipline could also lift investor confidence in Nigeria’s public finance reforms.

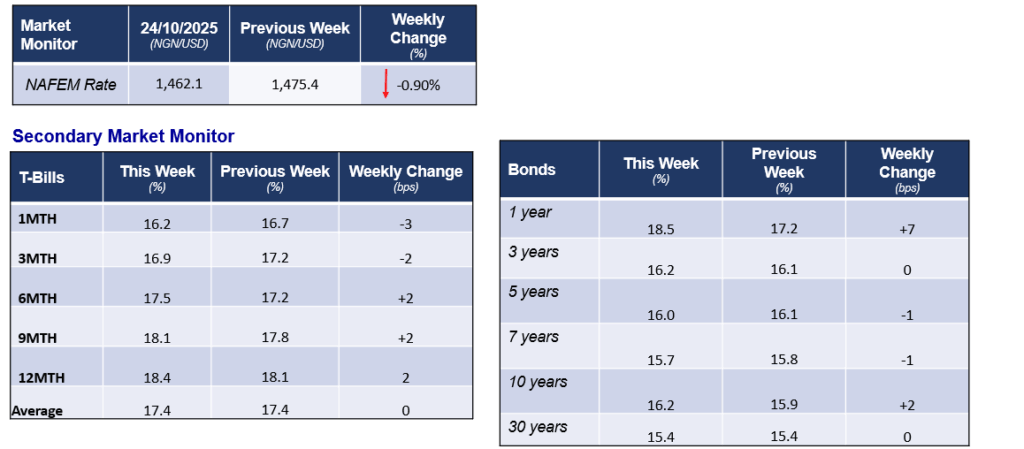

CBN Projects $20bn Current Account Recovery on Stronger Non-Oil Exports and FX Reforms

The Central Bank of Nigeria (CBN) projects that the country’s current account balance will recover by about USD20.0bn in the medium term, driven by rising non-oil exports, stronger external reserves, and improved FX liquidity. The outlook signals improving confidence in Nigeria’s external position, following a series of policy reforms focused on diversifying export earnings and enhancing transparency in the FX market. As at 22nd October 2025, gross external reserves stood at USD42.9bn.

A stronger current account position is positive for Nigeria’s macroeconomic outlook, as it should ease exchange rate pressures, reduce external borrowing needs, and strengthen the CBN’s intervention capacity in the FX market. For the fixed-income market, improved reserves and stronger external metrics could narrow sovereign risk premiums, supporting yield moderation over the medium term. Similarly, in the equities market, a more stable FX environment and sustained export growth may attract foreign portfolio inflows, particularly into consumer goods, industrials, and export-linked stocks.

In the near term, the CBN’s projection is likely to support investor sentiment, though actual performance will depend on consistent non-oil export growth, policy stability, and global commodity trends. While risks such as lower oil prices, slower global growth, or domestic production challenges could weigh on momentum, the outlook points to gradual external stability and improving fiscal resilience, supporting confidence in Nigeria’s ongoing macroeconomic recovery.

Dangote Refinery to Double Capacity to 1.4mbpd, Targeting Global Leadership in Refined Products

Dangote Oil Refinery has announced plans to expand its 650,000bpd refinery in the Lekki Free Zone to 1.40mbpd, which would make it the largest single-train refinery in the world. The expansion, described as a cloning project, will replicate the existing design to ensure faster execution and operational efficiency. Funding will come from Middle Eastern investment partnerships and a planned 5–10% public listing of the refinery business on the Nigerian Exchange (NGX), signaling a shift toward market transparency and capital diversification.

The refinery, which began operations in 2024, currently meets about 80.0% of Nigeria’s fuel demand, with surplus diesel and jet fuel exported to regional markets. To ensure steady crude supply, Dangote has secured crude-for-naira supply agreements with NNPC and is developing upstream assets (OML 71 & 72) capable of producing up to 40,000bpd. Although output has been affected by operational bottlenecks and maintenance downtime, efforts are ongoing to stabilize production ahead of the expansion phase.

In the near term, the project could boost FX liquidity, improve the current account balance, and reduce dependence on fuel imports, aligning with the CBN’s projection of a USD20.00bn current account surplus in 2025. Over time, increased refining capacity is expected to ease inflationary pressures, support energy security, and create jobs across logistics and industrial value chains.

While risks remain from potential cost overruns, crude supply disruptions, and expected global refining overcapacity by 2030, the expansion highlights Dangote’s strategic intent to position Nigeria as a regional energy hub and a major player in the global refined products market.

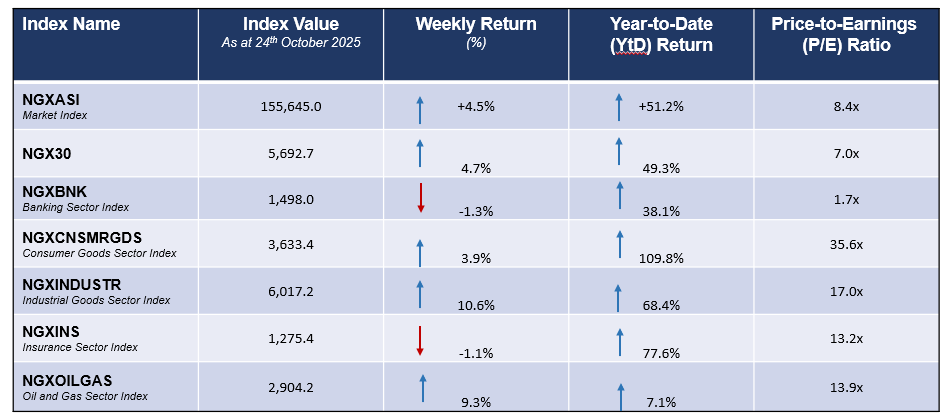

Equities Market – Sectorial Performance

Weekly Performance of Sectorial Indices

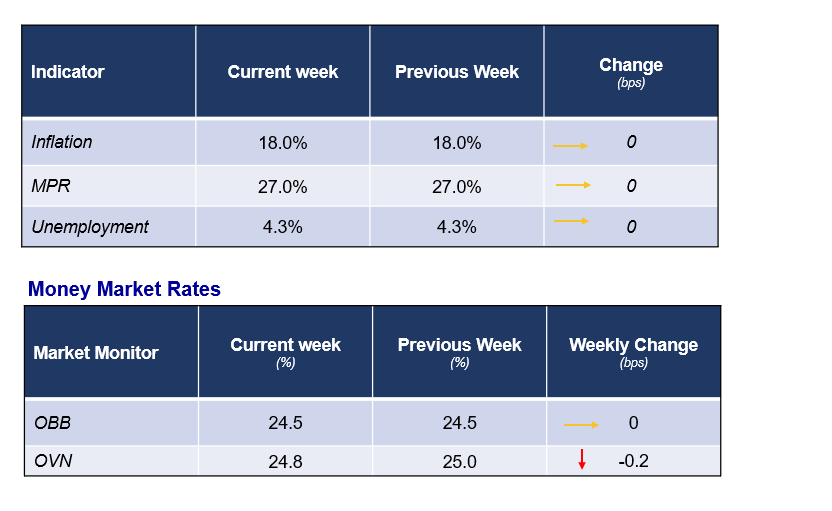

CBN OMO Auction Sees Weaker Demand as Bond and Eurobond Markets Extend Bullish Momentum

The Central Bank of Nigeria (CBN) conducted an OMO auction during the week, offering a total of NGN600.0bn across the 196-day and 252-day maturities. Investor demand moderated, with total subscriptions declining to NGN1.1trn, while the CBN allotted NGN827.0bn at stop rates of 19.5% and 19.8%, respectively.

In the secondary Treasury Bills market, sentiment turned bearish after weeks of sustained gains, as the average yield edged up by 5bps to 17.4% (from 17.3%). The sell-off was largely concentrated at the long end of the curve, with the MAY-26 maturity recording a notable 38bps increase. Conversely, the short- to mid-end segment witnessed mild yield compression, particularly on the FEB-26 (-9bps) and NOV-25 (-6bps) papers.

Meanwhile, the bond market sustained its bullish momentum, with the average yield declining by 10bps to 15.8% (from 15.9% previously). The rally was largely driven by buying interest in short- to mid-dated instruments, where notable yield contractions were observed on the APR-29 (-53bps), MAY-33 (-41bps), and JUN-33 (-67bps) maturities. Conversely, the belly of the curve remained relatively quiet, recording minimal yield movement.

The Eurobond market closed the week on a bullish note, as the average yield declined by 19bps to 7.8% (from 8.0%). The rally was broad-based across the curve, driven by renewed buying interest from offshore investors amid improved risk sentiment. Demand was particularly strong at the short end, with the NOV-25 paper leading gains after yields compressed by 29bps.

Market Snapshot

Macroeconomic Indicators