Nigeria’s PMI Climbs to 54.0pts in September, Signaling Stronger Economic Expansion Across Key Sectors

Global Macro Highlights

IMF Upgrades 2025 Global Growth Forecast Amid Stronger Economic Activity

The IMF has revised its 2025 global growth forecast upward to 3.2% from 3.0% in its June projection. This upgrade was attributed to the lower-than- expected tariff rates, strong global output supported by the front-loaded imports and rerouted supply chains which reduced the impact of the intense trade war earlier in the year. Also, fiscal stimulus in economies like Europe and China, with a surge in Al investment continued to boost productivity and spending. The improved growth outlook indicates that global economic activity and output remain resilient despite the uncertainties resulting from the trade war and geopolitical tensions. This upward revision also signals a stronger global demand and output, easing the fears of a sharp decline in global demand. Looking ahead, a stronger global economy growth may lead to slower pace of rate cuts by major central banks as strong activity could sustain inflationary pressures. Nonetheless, sustained demand favors Nigeria’s FX revenue.

China’s Inflation Shows Mixed Signals as Core Prices Rise Despite Persistent Deflationary Pressure

According to the National Bureau of Statistics, China’s Consumer Price Index (CPI) fell by 0.3% YoY in September 2025 (vs -0.4% in August), the second consecutive decline. The decline was driven by a 4.4% drop in food prices, as 17% slump in pork and lower vegetable prices drove the index lower. Meanwhile, core inflation rose 1.0% YoY, the highest since Feb 2024, supported by higher prices of gold jewelry, home appliances, and healthcare. The Produce Price Index (PPI) contracted 2.3% YoY (vs -2.9% in Aug), marking the slowest decline in seven months due to government efforts to curb industrial competition. On a month-on-month basis, CPI edged up 0.1%, while PPI was flat, indicating marginal demand recovery. Despite persistent deflationary pressures, stronger core inflation reflects improving demand, suggesting extension of government stimulus. Looking ahead, deflation is expected to persist but at a slow pace, though US-China trade tensions could weigh on consumer confidence and spending recovery.

Domestic Events

Nigeria’s Oil Output Declines on Strikes and Maintenance Shutdowns but Rebound Expected as Operations Resume

The Nigerian Upstream Petroleum Regulatory Commission (NUPRC) reported that crude oil production, including condensates, declined month-on-month for the second consecutive time by 3.1% to 1.6mbpd in September 2025, from 1.6mbpd recorded in August. The decline in output was attributed to the 3-day industrial strike by the PENGASSAN union, which temporarily stopped production activities, and the shutdown of key pipeline facilities including the Trans-Niger Pipeline, for maintenance purposes. Consequently, Nigeria did not meet its OPEC quota in September, as crude oil production alone stood at 1.4mbpd compared top the 1.5mbpd quota. However, crude oil production increased marginally by 1.6% YoY as improved security supported overall volumes compared to September 2024. The decline in oil production is expected to weigh on export and fiscal revenues, as lower output in September and oil prices being low may impact export receipts. Looking ahead, with the strike and other disruption resolved and production resuming, we expect a rebound in oil output in the near term supported by the improved security measures in the oil producing regions.

Dangote Cement Expands West African Footprint with New 3.0Mta Côte d’Ivoire Plant

Dangote Cement has begun operations at its new plant in Attingue, Côte d’Ivoire which has an installed capacity of 3.0mn tonnes per annum (Mta). This new plant makes Côte d’ivoire the 11th African country to host a Dangote production site, boosting the group’s total capacity to 55Mta. The plant is expected to support growing demand for construction materials driven by rapid urbanization and large-scale infrastructure projects across the country, while also reducing Côte d’Ivoire’s reliance on cement imports. Since the announcement, Dangote Cement’s stock has gained 4.4%, as investors reacted positively to the commencement of operations. Going forward, we expect investors to shift focus toward the company’s 9M:2025 earnings release Looking ahead, this expansion is expected to strengthen Dangote Cement’s West African footprint and support volume and revenue growth in the near term. However, competitive pricing and elevated logistics costs may temporarily pressure margins as operations stabilize.

Nigeria’s PMI Climbs to 54.0pts in September, Signaling Stronger Economic Expansion Across Key Sectors

According to the National Bureau of Statistics (NBS), Nigeria’s headline inflation eased for sixth consecutive month to 18.0% YoY in September 2025 from 20.1% in August. This was driven by decline in both food and core inflation. Food inflation fell sharply to 16.9% YoY (from 21.9% in August), due to peak harvest season on some key staples like local rice and potato while core inflation declined to 19.5% YoY (from 20.3% in August), reflecting slower price growth across major categories such as health, transport, and clothing & footwear. Month-on-Month, headline and core inflation eased slightly to 0.7% MoM and 1.4% MoM respectively (vs. 0.7% and 1.4%). Also, food prices deflated for the first time since February 2012, as a result of the strong impact of the ongoing harvest season on market supply. Looking ahead, we expect food inflation to ease further supported by the ongoing harvest season and government incentives in the Agric sector. We also expect core inflation to be relatively steady supported by the sustained FX stability. Overall, we foresee a continued disinflationary trend in the headline inflation.

IMF Raises Nigeria’s Growth Outlook to 3.9% for 2025 on Stronger Macroeconomic Stability and Oil Output

The IMF upgraded its growth forecast for the Nigerian economy in 2025 to 3.9% from 3.4% and its 2026 growth outlook was also revised upward to 4.2% from the 3.3% previous forecast. The 2025 upward revision was attributed to stronger macroeconomic stability, rising investor confidence and increased oil output, with crude oil and condensates averaging 1.7mbpd in Jan-Sept 2025 (vs. 1.5mbpd in Jan-Sept 2024). Meanwhile, the 2026 growth outlook was supported by reduced domestic uncertainties and Nigeria’s limited exposure to the tariffs imposed by the US, which have had minimal impact on the domestic economy. The recent GDP rebasing was noted to enhanced coverage of economic activities, thereby providing a more accurate measurement of overall economic activity. The stronger growth outlook by IMF could further strengthen investor and business confidence, thereby supporting more capital inflow and productivity. Looking ahead, we expect on going growth momentum to persist, supported by improved oil production volumes, increased productivity across key sectors such as services and agriculture, and continued macroeconomic stability.

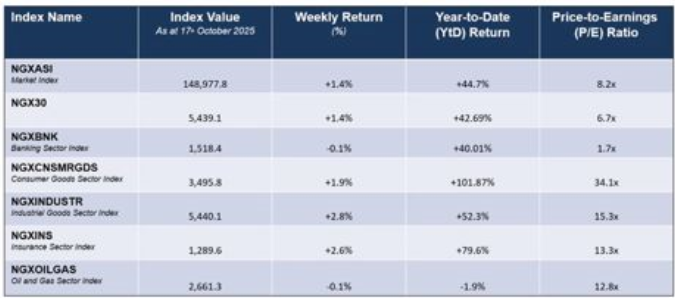

Equities Market – Sectorial Performance

Weekly Performance of Sectorial Indices

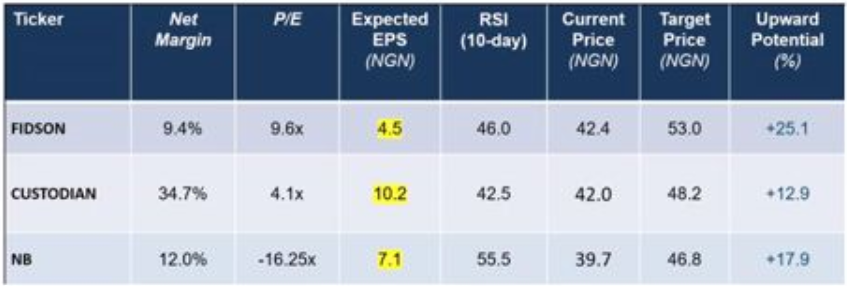

Stocks Top Picks For The Week

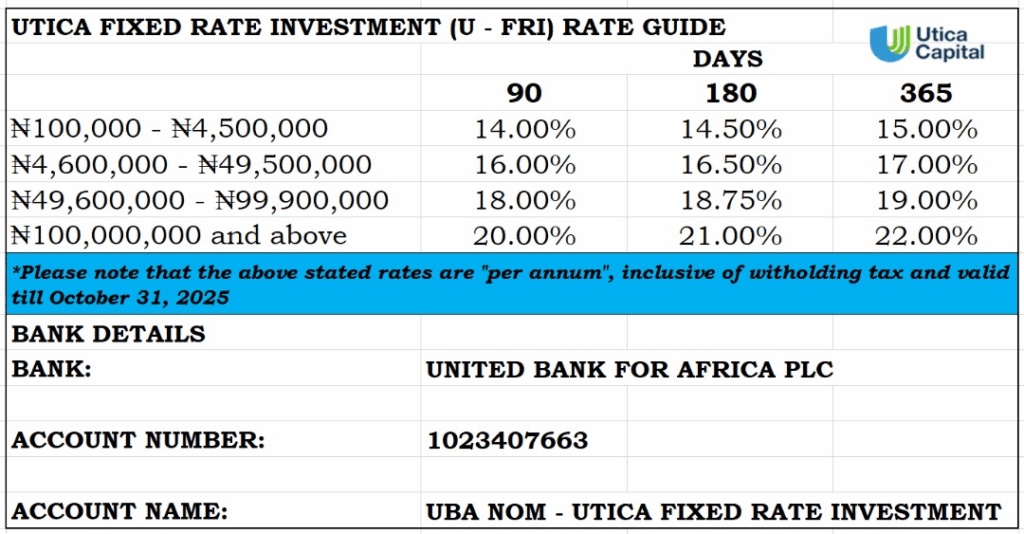

Fixed Income Opportunities for the week