Nigeria’s Trade Surplus Hits 3-Year High in Q2:2025

Global Macro Highlights

Rising U.S. Food Costs Push Inflation Higher, Boosting Odds of Fed Rate Cut

U.S. consumer prices rose by 0.4% MoM in August, the highest increase since January, lifting headline CPI to 2.90% YoY. The surge was driven by food costs (+0.5% MoM, +0.6% in supermarkets) with food inflation accelerating to 3.20% YoY from 2.90% in July, while core inflation held steady at 3.10%.

Tariff pass-through and farm labor shortages continue to fuel higher food prices, eroding household purchasing power and keeping borrowing costs elevated. With unemployment climbing to 4.30% (highest since 2021) and job losses recorded in June, labor market weakness is amplifying pressure on the Fed’s decision.

While inflation remains sticky, the softening jobs backdrop makes a 25bps rate cut increasingly probable as policymakers seek to support employment while containing inflation expectations.

ECB Holds Rates at 2.00% Amid Trade Tensions and Weak Demand

The European Central Bank (ECB) kept its benchmark rate unchanged at 2.00% for the second consecutive meeting, following a cut in June 2025 from last year’s record high of 4.0%. Inflation has hovered slightly above target, fluctuating between 2.0%-2.5% since January, as persistent global trade tensions, including the recently imposed 15.0% U.S. tariffs on EU exports, continue to weigh on the outlook.

We expect the ECB to keep rates on hold, with cuts unlikely before late 2025 unless growth falters, while further hikes are off the table amid moderating inflation and weak demand.

China’s CPI Falls 0.4% YoY in August, Extending Deflation Risks to Growth

China’s inflationary pressures softened in August, with CPI declining by 0.40% YoY after remaining flat in July, marking the sharpest contraction since February (-0.70%). At the same time, producer prices fell 2.90% YoY, extending the deflationary trend that has persisted since late 2022.

The weakness largely reflects high base effects from last year’s elevated food costs and muted seasonal demand, underscoring the fragility in household spending and broader domestic activity. Sustained deflation poses a risk to Beijing’s 5.00% growth target, dampens investor confidence, and highlights structural demand imbalances.

CPI is projected to stay negative through Q3:2025, with a modest recovery likely in Q4 as stimulus measures filter through and base effects ease. Policy support is expected to remain targeted rather than broad-based, emphasizing consumer and SME subsidies.

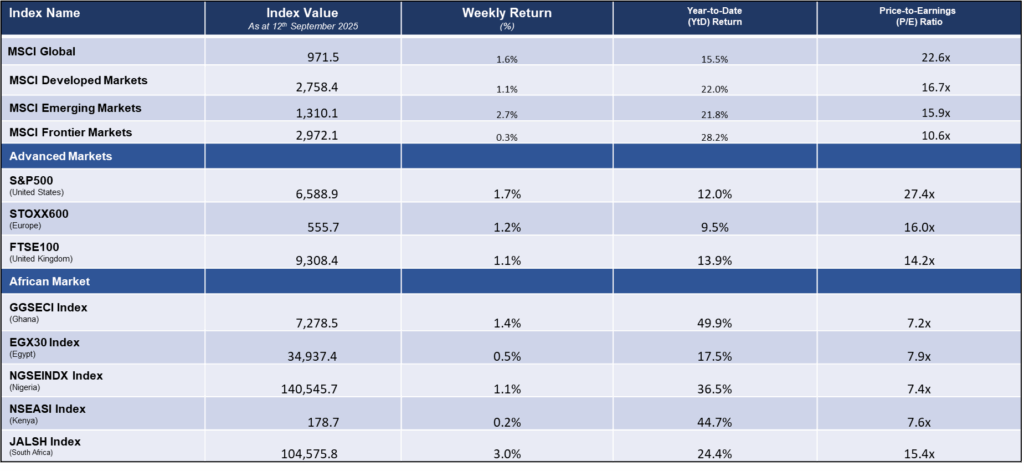

Global Equities Market

Weekly Performance of Major Global Indices

Domestic Events

Nigeria’s Trade Surplus Hits 3-Year High in Q2:2025

Nigeria’s trade surplus surged by 44.3% QoQ to NGN7.46trn in Q2:2025, its strongest in nearly three years, as buoyant exports outpaced weaker imports. Total exports rose 10.5% QoQ to NGN22.75trn, led by non-crude petroleum products (NGN7.74trn) and non-oil exports (N3.05tn, 13.4% of total).

Manufactured exports were a standout, up by 173% QoQ to NGN803.8bn, while imports slipped 0.9% to NGN15.29trn, with Asia and China dominating supply, largely machinery, refined petroleum, and wheat. Spain remained Nigeria’s top export destination, followed by India and France, with Europe absorbing 38% of shipments.

The surplus provides FX relief, though reliance on petroleum (85% of exports) leaves Nigeria exposed to external shocks. Gradual gains in manufactured and mineral exports highlight early progress on diversification, but the heavy import bill underscores persistent structural dependence.

FG, EU, and Germany Launch €18.3m Project to Boost Nigeria’s Agro Value Chains

The Federal Government, with Germany and the EU, has launched the EUR18.30mn EU-VACE TARED Project (2024–2028), targeting cocoa, dairy, tomato, and ginger value chains in Cross River, Kano, Kaduna, Kebbi, Ondo, Oyo, and Plateau.

The programme aims to reduce post-harvest losses by 15.00%, boost incomes and turnover by 15.00%, create 10,000 jobs, and channel EUR2.00mn in financing, especially to women and youths, while aligning exports with EU deforestation standards.

The project is expected to support small and medium farmers by improving supply chain efficiency and reducing losses.

NUPRC Secures $400m in Decommissioning Liabilities, Approves $4.4bn Plans

The Nigerian Upstream Petroleum Regulatory Commission (NUPRC) has secured over USD400mn in pre-sale decommissioning and abandonment (D&A) liabilities and approved 94 D&A plans worth USD4.4bn since April 2023, ensuring oil asset divestments do not leave Nigeria with stranded environmental or financial burdens.

Acting under the Petroleum Industry Act and drawing from global precedents, NUPRC enforced escrow accounts and Letters of Credit before asset transfers, while deals involving Oando, Seplat, Renaissance Africa Energy, and Telema Energies underwent strict assessments. Host community trusts worth over USD9.2mn were embedded, supported by NEITI oversight, OPTS engagement, and a new escrow domiciliation framework.

These measures boost regulatory credibility, safeguard host communities, and provide investor clarity in the short to medium term, while positioning Nigeria as a regional model for responsible divestments over the long run. Success will hinge on consistent enforcement and political continuity.

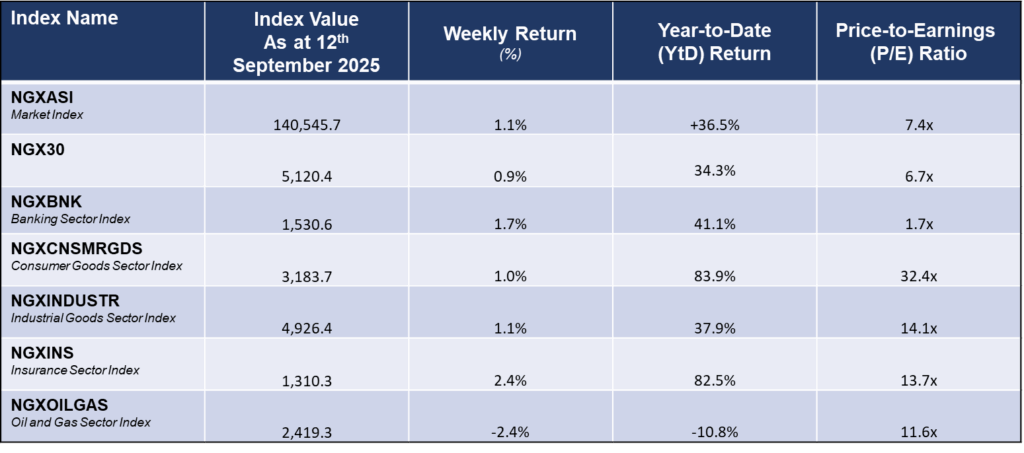

Equities Market – Sectorial Performance

Weekly Performance of Sectorial Indices

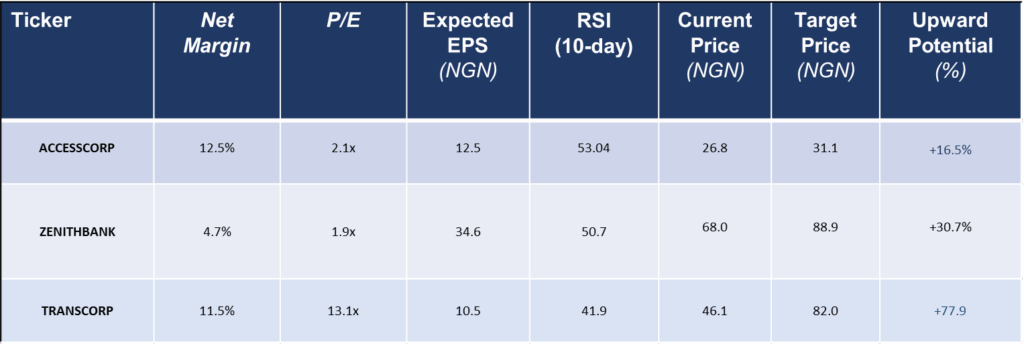

Stocks Top Picks for the Week

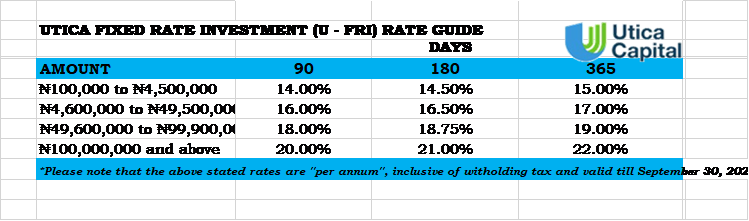

Fixed Income Opportunities for the week