IMF Upgrades Nigeria’s Growth Forecast Amid Oil Gains & Reform Progress

Global Macro Highlights

U.S. Revives Tariffs, Global Trade Faces New Jitters Amid Fragile Recovery

This week, the United States reinstated tariffs ranging from 10.0% to 50.0% on imports from 69 countries under former President Trump’s revived reciprocal trade policy. A baseline tariff of 10.0% was imposed on goods from the United Kingdom, while Canada faced a 35.0% rate, reportedly linked to continued drug trafficking concerns. Brazil was hit with the steepest rate at 50.0%, while South Africa and Nigeria were levied with 30.0%and 15.0% tariffs, respectively. The U.S. and EU reached a partial trade agreement. Under the new deal, the U.S. will cap tariffs on most EU goods at 15.0%, down from the initially proposed 30.0%, providing relief particularly for European auto exporters.

Meanwhile, the U.S. economy showed signs of recovery, with GDP rising by 3.0% year-on-year in Q2:2025 after a 0.5% contraction in the previous quarter. However, this rebound was largely driven by a sharp 30.3% drop in imports, which flattered the headline figure and suggests underlying softness in domestic demand. Inflation remains elevated, in part due to lingering effects of earlier tariff rounds and supply chain shifts. As a result, the Federal Reserve held interest rates steady at 4.25%-4.50% and indicated no imminent rate cuts, emphasizing the need for sustained disinflation before policy easing can be considered.

We expect trade frictions to intensify, especially with emerging markets that lack leverage to negotiate exemptions or reciprocal benefits, while headline GDP growth may remain resilient in the short term, weak consumer spending and cautious corporate investment could weigh on momentum in H2:2025.

IMF Lifts Global Growth Outlook, But Trade Tensions Threaten Momentum”

The International Monetary Fund (IMF) has revised its global growth forecast for 2025 upward to 3.0%, from its earlier projection of 2.8%. This upgrade reflects a temporary boost in global trade, as firms accelerated imports ahead of newly imposed U.S. tariffs. While modest, the upward revision underscores a stronger-than-expected macroeconomic performance in the first half of the year and signals cautious optimism for the global economy. Short-term momentum was also supported by looser financial conditions, a softer US dollar, and fiscal stimulus in some economies. However, the broader backdrop remains clouded by renewed trade tensions. Although the average US tariff rate declined from 24.0% to 17.3%, policy uncertainty remains elevated, keeping global trade dynamics on edge.

Looking ahead, we expect global growth to slow down as the temporary boost from front-loaded imports fades. Underlying demand remains weak, and persistent inflation, coupled with unresolved trade disputes, continues to weigh on business confidence and investment flows. With mounting pressures across advanced economies, the recovery trajectory is expected to be fragile, uneven, and increasingly vulnerable to external shocks.

SARB Cuts Rates Again, Signals Shift Toward Lower Inflation Target

At its latest policy meeting on Thursday, the South African Reserve Bank (SARB) lowered the benchmark repo rate by 25 basis points to 7.00%, marking the third consecutive rate cut this year, bringing the total reduction to 75bps. This move reflects growing confidence in the inflation outlook, with headline inflation easing to 3.0% in June and core inflation at 2.9%, both well within the SARB’s 3.0–6.0% target range.

This rate cut is aimed at easing borrowing costs for households and businesses, potentially boosting consumer spending and investment especially as economic activity weakens. Notably, the SARB also indicated a strategic shift, aiming to anchor inflation closer to the lower end of its target band (3.0%), rather than the previous medium-term midpoint of 4.0%. This suggests a more accommodative policy stance going forward.

Still, with ongoing global tariff tensions posing inflationary risks, we expect the SARB to maintain a cautious approach, balancing support for growth support whilst keeping an eye on possible triggers to inflation in the near term.

Ghana Delivers Historic Rate Cut as Inflation Falls to 2-Year Low

Ghana’s Central Bank has slashed its benchmark interest rate by 300 basis points to 25.0% from 28.0%, this is the largest rate cut in the country’s history. The monetary authority indicated that the deceleration in prices levels had been underpinned by the bank’s tight monetary policy stance. Headline inflation dropped to 13.7% in June from 18.4% in May, its lowest level since December 2021 driven partly by the appreciation of the Cedi, due to the surge in gold prices– being one of Africa’s top gold exporter, this boosted foreign exchange reserves. Additionally, improving macroeconomic fundamentals has contributed to the easing inflation pressures in the country.

We expect this significant rate cut to spur economic activity through lesser borrowing costs, boosting consumer spending, and improving credit access for businesses. While the decision signals growing confidence in disinflation trend, policymakers remain wary of upside risks linked to utility prices and elevated food prices and with this we expect Ghana’s central main a cautious policy stance in the near term.

Global Equities Market

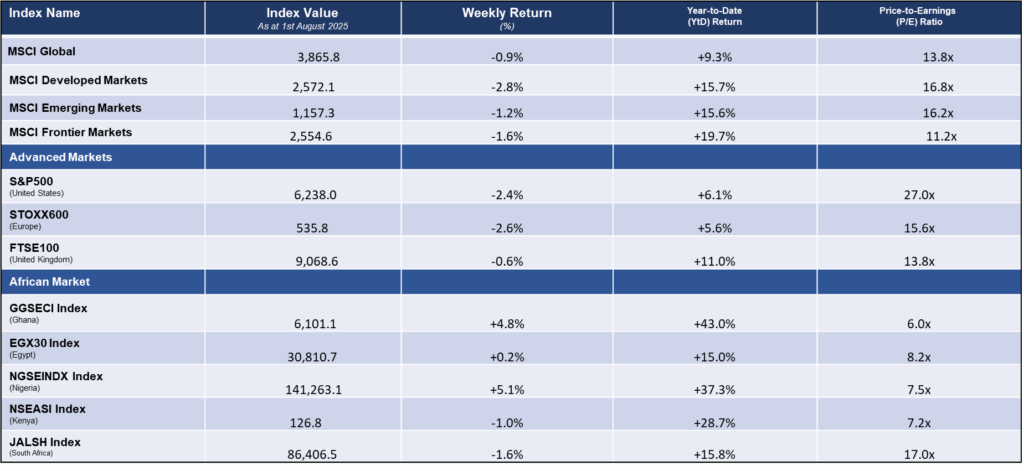

Weekly Performance of Major Global Indices

Domestic Events

IMF Upgrades Nigeria’s Growth Forecast Amid Oil Gains & Reform Progress

The IMF has revised Nigeria’s 2025 GDP growth projection upward to 3.4% from 3.0% and raised its 2026 forecast to 3.2% from 2.7%. The upgrade reflects growing optimism around Nigeria’s economic trajectory, backed by tangible improvements across key sectors and early gains from ongoing macroeconomic reforms.

According to the IMF, the upward revision is underpinned by stronger oil production, improved performance in the services sector, and gradual progress on critical structural reforms. Crude oil output averaged 1.68mbpd in H1:2025 (its highest in years), driven by enhanced security in the Niger Delta, renewed upstream investments, and higher export receipts. Additionally, the gradual ramp-up in local refining capacity has helped reduce pressure on the FX market. They also highlighted signs of recovery in non-oil sectors, particularly following the GDP rebasing exercise.

While the growth outlook appears more promising, we maintain a cautiously optimistic stance. Fiscal vulnerabilities remain, especially with oil prices trading below the government’s benchmark of USD75.00pb and continued geopolitical risks could cloud the recovery path. Nonetheless, this IMF revision may boost investor sentiment and reinforce confidence in Nigeria’s medium-term prospects.

Coca‑Cola Exits CHI Limited, UACN Steps In – A Strategic Shake-Up in Nigeria’s FMCG Space

Coca‑Cola has reached an agreement to sell its stake in CHI Limited (the maker of household brands like Chivita and Hollandia) to UAC of Nigeria Plc (UACN). The deal is part of Coca‑Cola’s global pivot toward an asset-light strategy, aimed at sharpening its focus on high-growth, high-margin categories while reducing operational exposure in emerging markets.

Despite stepping away from direct ownership, Coca‑Cola reaffirmed its long-term commitment to Nigeria, pledging potential investments of up to USD1.0bn over the next five years, although contingent on improving macroeconomic stability.

For UACN, the acquisition is a strategic leap, strengthening its position in Nigeria’s FMCG sector, especially within the juice and dairy segments where CHI commands notable market share. The move is also expected to enhance UACN’s product diversification and consolidate its presence in key consumer categories. We however note that this deal is subject to regulatory approval.

Agri-Firms PRESCO & Ellah Lakes Eye ₦500bn Equity Raise to Accelerate Growth

During the week, PRESCO Plc, a leading integrated palm oil producer, announced plans to raise NGN250bn through a rights issue. The capital raise is aimed at expanding the company’s production capacity, particularly through the acquisition of additional biological assets. If fully subscribed, the issuance will significantly boost PRESCO’s asset base(currently valued at NGN613.0bn) and provide much-needed liquidity for its growth ambitions. However, the rights issue also presents potential dilution risks for shareholders who may not exercise their rights.

In a similar move, Ellah Lakes Plc disclosed its intention to raise NGN250bn in equity capital through a private placement, public offer, or any other suitable equity issuance vehicle, following board approval. With a current asset base of NGN24.9bn, the capital injection, if successful, would materially strengthen Ellah Lakes’ balance sheet and elevate its competitive position in the domestic agriculture landscape.

Together, these developments underscore a renewed optimism in Nigeria’s agriculture sector, as companies position themselves for mid-to-long-term growth. For PRESCO, the additional capital could enhance its ability to meet both export and domestic demand for oil palm products, while Ellah Lakes’ planned raise could support expansion and strategic initiatives to grow market share locally and internationally.

Equities Market – Sectorial Performance

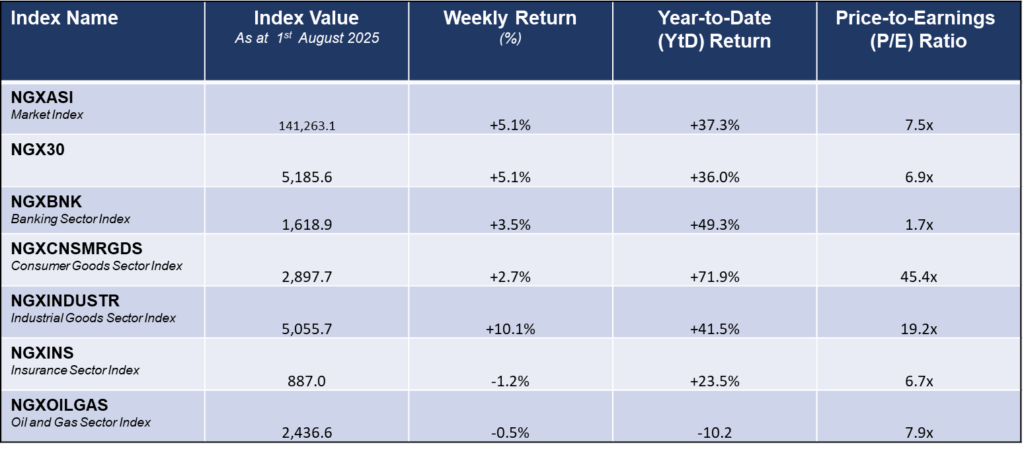

Weekly Performance of Sectorial Indices

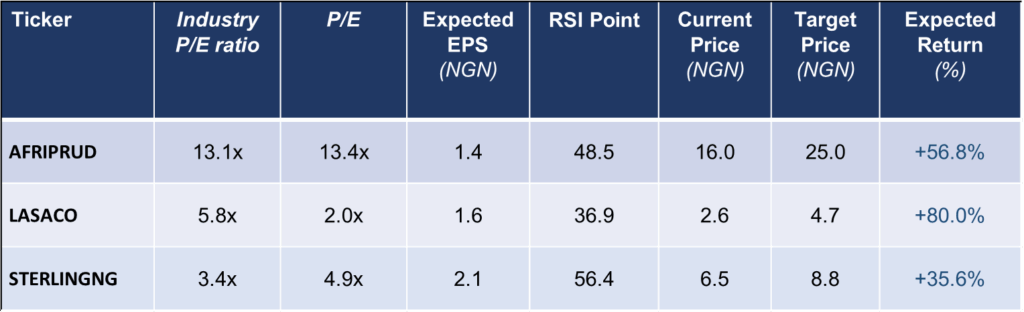

Stocks Top Picks for the Week

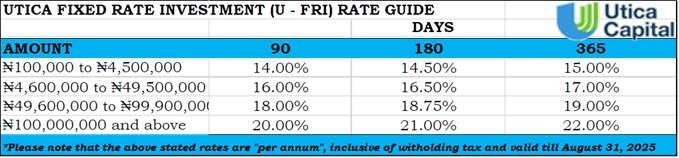

Fixed Income Opportunities for the week