MPC Holds Rates Steady to Balance Inflation Control and Growth Amid Global Uncertainty

Global Macro Highlights

U.S.–Japan Trade Deal Boosts Markets, Sets Stage for Auto Sector Shake-Up

The United States finalized a trade deal with Japan during the week, with Japan pledging a USD 550bn investment into the U.S. economy. In return, the U.S. agreed to cut tariffs on Japanese imports, especially vehicles and auto parts, while steel and aluminum remain excluded. The agreement averted a planned 25–27.5% tariff hike, boosting investor confidence. Japanese auto stocks like Toyota and Honda surged, alongside gains in the Nikkei 225, S&P 500, and FTSE 100.

Looking ahead, we expect Japanese export volumes especially in the auto sector to rise, supporting a rebound in business activity that could help offset Japan’s 0.2% GDP contraction in Q1 2025. While global equities may continue to benefit from the de-escalation, U.S. auto manufacturers may face intensified competition from Japanese imports, potentially weighing on domestic output and margins.

ECB Pauses Rate Cuts as Inflation Hits Target and Eurozone Outlook Steadies

At its fifth meeting of the year, the European Central Bank (ECB) held its key interest rate at 2.15% and the deposit rate at 2.00%, marking a pause in the easing cycle that began in mid-2024. The decision reflects a slowdown in headline inflation, which fell to 2.0% in June, alongside broadly stable economic conditions across the Eurozone.

The pause suggests funding costs will remain steady, offering room for improved business activity. Given disinflationary trends in major economies like Germany and inflation now aligned with the ECB’s 2% target, we expect rates to stay on hold in the near term. Further cuts appear unlikely unless growth weakens materially or inflation decelerates more sharply.

South Africa’s Inflation Edges Up but Stays Within Target, Keeping Rate Cuts in Play

South Africa’s headline inflation rose to 3.0% YoY in June, from 2.8% in May, remaining well within the South African Reserve Bank’s 3–6% target range. The slight uptick was driven by higher food, rent, and utility costs, despite a decline in fuel prices. On a monthly basis, inflation rose 0.2%.

Importantly, this modest increase does not disrupt the broader disinflationary trend that has prevailed over the past year. Inflation has stayed below the SARB’s 4.5% midpoint target since August 2024, creating room for a series of rate cuts to support a sluggish economy.

Looking ahead, price levels are expected to remain stable, though rising energy costs and geopolitical tensions could pose upside risks. With inflation still contained and domestic demand weak, we expect the SARB to maintain its accommodative stance, albeit at a slower pace of easing.

Global Equities Market

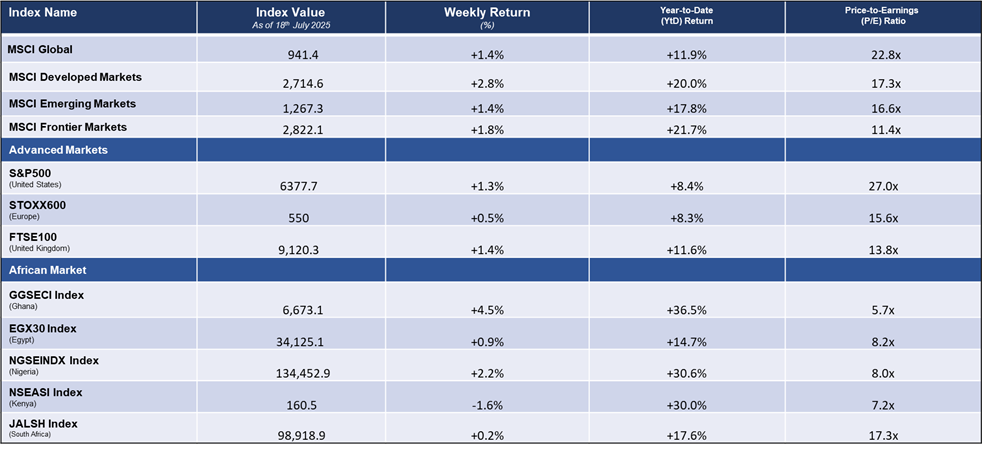

Weekly Performance of Major Global Indices

Domestic Events

Nigeria’s Rebasing Lifts Q1 GDP to 3.1% YoY, Driven by Strong Non-Oil Sector Performance

Following the GDP rebasing, the National Bureau of Statistics reported that Nigeria’s economy grew by 3.1% YoY in Q1:2025, up from 2.3% in Q1:2024, with total output reaching NGN49.34trn. Growth was driven by the non-oil sector, which rose 3.19% YoY, led by Telecoms (+7.8%), Financial Institutions (+15.9%), Crop Production (+3.7%), Real Estate (+4.6%) and Trade (+1.78%).

The oil sector posted moderate growth of 1.9%, down from 4.7% in Q1:2024, despite a rise in output to 1.62mbpd. The weaker growth reflects base effects from last year’s higher performance.

MPC Holds Rates Steady to Balance Inflation Control and Growth Amid Global Uncertainty

The Monetary Policy Committee (MPC), in its July meeting, held all key policy parameters steady for the third consecutive time maintaining the MPR at 27.5%, CRR at 50.0% for Deposit Money Banks and 16.0% for Merchant Banks, and the Liquidity Ratio at 30.0%. This decision was informed by the moderation in inflation and the need to manage government borrowing costs, while also keeping an eye on external risks such as global trade tensions and supply chain disruptions.

Going forward, the MPC’s decision is expected to support real sector growth by fostering monetary stability and a more predictable FX environment which could improve business activities.

Senate Approves $21.5bn Loan Plan to Boost FX Liquidity and Infrastructure Amid Debt Concerns

The Nigerian Senate approved the federal government’s 2025–2026 borrowing plan, comprising USD21.5bn, EUR2.2bn, JPY15bn, and a EUR65mn grant. It also approved a NGN757.9bn domestic bond to settle pension arrears, plus plans to raise USD2bn in FX-denominated local debt to ease reserve pressure. Funds will support key sectors like agriculture, power, housing, and digital infrastructure, and are expected to boost FX liquidity and reduce exchange rate volatility.

However, with total debt at NGN149.39trn and external debt at USD45.9bn (47.3%), rising debt service costs could pressure public finances and heighten debt sustainability risks.

Access Bank Acquires AfrAsia Stake to Deepen Offshore Presence and Expand African Trade Links

Access Bank has acquired a 76% stake in AfrAsia Bank, a top Mauritian financial institution, as part of its global expansion strategy. The move aims to establish Mauritius as a hub for trade finance, private banking, and cross-border services across Africa and key global markets.

The acquisition is expected to diversify earnings and strengthen offshore operations, though its success will depend on effective integration and compliance across jurisdictions.

Equities Market – Sectorial Performance

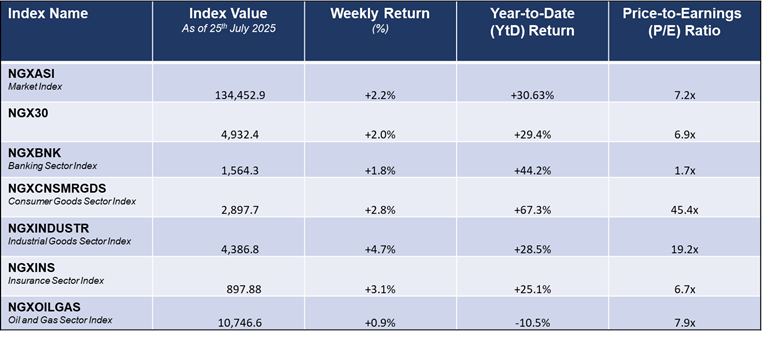

Weekly Performance of Sectorial Indices

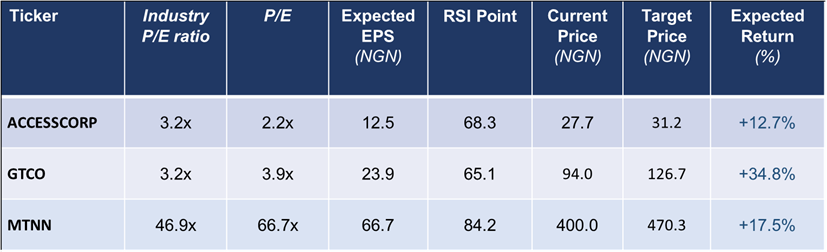

Stocks Top Picks for the Week

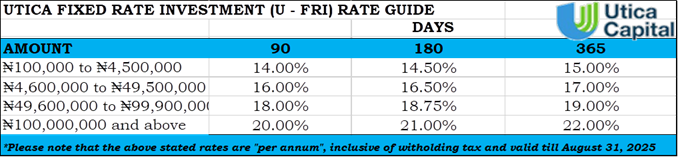

Fixed Income Opportunities for the week