Eurozone Inflation Falls Below ECB Target, Opening Door for Potential Rate Cuts

Global Macro Highlights

Fed Holds Rates Steady Amid Inflation Worries and Global Tensions

The U.S. Federal Reserve kept its benchmark interest rate unchanged at the 4.25%-4.50% range, maintaining a cautious stance amid persistent economic uncertainty. This decision reflects concerns over lingering inflationary pressures, especially those stemming from newly imposed U.S. tariffs on Chinese imports and the potential economic fallout from ongoing tensions in the Middle East. By holding rates, the Fed aims to ensure inflation continues on a downward path. However, this approach could dampen economic activity in the near term, as elevated borrowing costs may weigh on consumer demand, business investment, and overall credit conditions. This is also expected to weigh on economic growth in the second half of the year.

BOE Holds Rates as Food Inflation Surges Despite Overall Price Slowdown

According to the Office for National Statistics (ONS), UK inflation eased marginally to 3.4% YoY in May 2025, down from 3.5% YoY in April. The slight moderation was largely attributed to lower transport costs, particularly a decline in airfares. However, underlying inflationary pressures persist, as food inflation accelerated to 4.4% YoY (vs 3.4% in April) reaching its highest level in over a year, driven by rising prices of bakery products, chocolate, and vegetables. Core services inflation also edged higher, climbing to 4.7% YoY from 4.5% in the previous month.

Against the backdrop of elevated global oil prices—fueled by geopolitical tensions in the Middle East—and persistent inflation, the Bank of England (BOE) opted to keep its benchmark interest rate unchanged at 4.25% during its June 2025 policy meeting. The decision underscores the Bank’s cautious stance as it weighs inflation risks against emerging signs of labour market softness. We expect the BOE to maintain this cautious stance in the near term. Unless there is a clear and sustained improvement in core inflation metrics and labour market slack becomes more pronounced, we do not foresee a rate cut in the next MPC meeting.

Eurozone Inflation Falls Below ECB Target, Opening Door for Potential Rate Cuts

According to Eurostat, Eurozone annual inflation eased to 1.9% YoY in May 2025, down from 2.2% YoY in April. The decline brings inflation just below the European Central Bank’s (ECB) 2.0% target for the first time since September 2024. The slowdown was largely driven by a sharp decline in energy prices ( -3.6% YoY vs 3.6% YoY) and services costs (3.2% YoY vs 4.0 YoY), which continued to offset upward pressure in food (3.2% YoY vs 3.0% YoY). Core inflation, which excludes volatile components such as energy, food, alcohol, and tobacco, also dropped to 2.3% (from 2.7% in April). We note that this sustained moderation in inflationary pressures gives the ECB more room to consider additional rate cuts. However, we expect the central bank to take a cautious stance in their next meeting, due to the global tensions, particularly linked to energy price volatility and uneven demand.

PBoC Holds Rates Steady to Gauge Impact of May Cut Amid Deflation Risks

The People’s Bank of China (PBoC) left both the 1-year and 5-year Loan Prime Rates (LPR) unchanged at 3.0% and 3.5% respectively. This decision followed a 10bps rate cut in May—the first since October 2024—and reflects the central bank’s intention to assess the transmission of recent policy easing before taking additional action. The pause aligns with the PBoC’s broader objective of maintaining financial stability while continuing to support weak domestic demand and deflationary pressures.

We expect the PBoC to maintain its current policy rates in the near term, while remaining flexible to deploy further liquidity easing if deflation deepens or credit demand weakens.

BoJ Holds Rates as Inflation Stays Elevated Amid Rising Food and Energy Costs

Japan’s annual inflation moderated to 3.5% YoY in May from 3.6% YoY in the previous month. While this marks a marginal deceleration, it remains well above the Bank of Japan’s (BoJ) 2.0% inflation target, reinforcing concerns around the stickiness of price pressures in the economy. The modest easing was primarily driven by softer inflation in discretionary categories such as clothing (2.6% YoY vs 2.7%), household items (3.6% YoY vs 4.1% YoY), and healthcare (2.0% YoY vs 2.2% YoY). However, the overall disinflationary trend was offset by significant increases in food prices, which rose 6.5% YoY, largely driven by a surge in rice prices, amid domestic supply constraints and elevated input costs. Also, prices of electricity (11.3% YoY vs 13.5% YoY) and gas (5.4% YoY vs 4.4% YoY) remain elevated. Moreover, the core index inched higher to 3.7% YoY (vs 3.5% YoY), its highest level since January 2023 (4.2% YoY). Meanwhile, on a monthly basis, inflation accelerated to 0.3% MoM, compared to 0.1% MoM in the previous month.

In response to underlying price pressure, the BoJ kept its policy rate unchanged at 0.5%. This decision also reflects concerns regarding escalating geopolitical risks and lingering uncertainty over trade policies, particularly from the U.S. We expect the BoJ to maintain its current policy stance in the near term as it seeks to balance the risk of overheating domestic inflation with growing external uncertainty.

SARB Likely to Hold Rates as Inflation Stays Below Target Amid Weak Demand

South Africa’s headline inflation remained at 2.8% YoY in May 2025, matching April’s print and remaining comfortably below the South African Reserve Bank’s (SARB) 3–6% target range. Price pressures intensified in food and non-alcoholic beverages (4.8% YoY vs 4.0% previously) driven by elevated prices in meat, dairy, and grains. Similarly, housing and utilities inflation edged slightly higher to 4.5% YoY (vs 4.4%) and clothing and footwear rose modestly to 1.3% YoY (from 1.2%). However, these increases were counterbalanced by easing in other categories like alcoholic beverages and tobacco ( 4.3% YoY vs 4.7%) and restaurant and accommodation services (1.8% YoY vs 3.0%). More importantly, transport inflation fell sharply (–4.8% YoY vs –3.9% in April, reflecting the lagged impact of lower fuel prices and base effects. Meanwhile, core inflation remained unchanged at 3.0% YoY, while on a monthly basis, inflation eased to 0.2% MoM, compared to 0.3% in April.

With headline inflation trending near the lower bound of SARB’s target range, and real sector data pointing to subdued domestic demand and weak credit uptake. We expect the SARB to take a cautionary stance, likely prioritizing inflation expectation and exchange rate stability, while monitoring external vulnerabilities, particularly in the face of heightened geopolitical risks, before signaling any shift towards policy easing.

Fitch Upgrades Ghana to B- as Reforms and Inflation Drop Boost Investor Confidence

Fitch Ratings upgraded Ghana’s long-term foreign-currency issuer default rating from CCC to B-, marking a significant shift in investor sentiment toward the West African nation. The outlook was also revised to Stable, signaling confidence in Ghana’s macroeconomic stabilization efforts. This upgrade follows a steady decline in inflation — from a peak of 54.1% in December 2022 to 18.4% as of its latest reading— supported by a combination of monetary tightening, fiscal consolidation, and ongoing IMF-backed reforms begin to bear fruit. The country’s adherence to its debt restructuring program and improved external balances have also played a key role in restoring market confidence. The move signals a potential turning point for Ghana, which defaulted on its external debt in 2022 amid a severe economic crisis. While the B- rating remains below investment grade, the upgrade could improve the country’s access to external financing and reduce sovereign borrowing costs over time. However, sustained reforms, clarity on external debt negotiations, and resilience in global commodity prices will be crucial for maintaining the momentum.

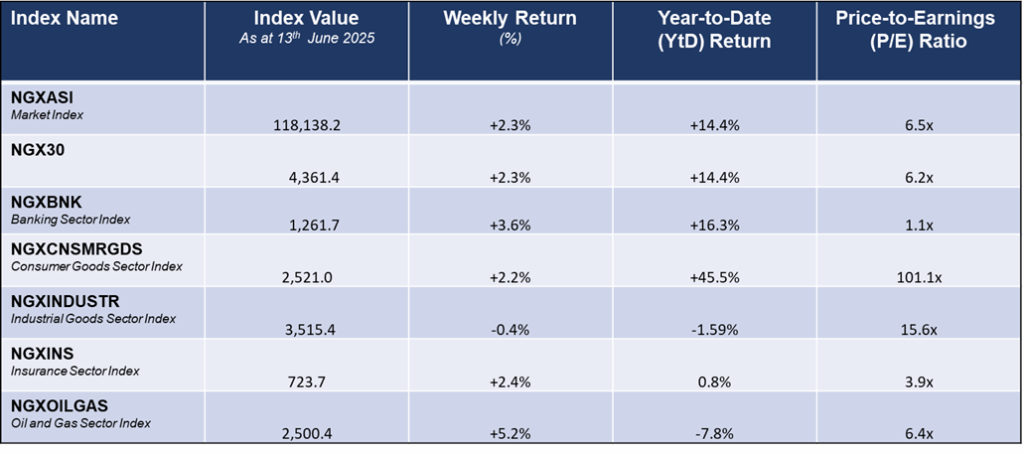

Equities Market – Sectorial Performance

Weekly Performance of Sectorial Indices

Domestic Events

Dangote Refinery to Ship First Gasoline Cargo to Asia, Marking Global Breakthrough

In a major step toward establishing Nigeria as a global player in refined fuel exports, the Dangote Refinery is set to ship its first gasoline cargo to Asia. The 90,000 metric ton shipment, arranged by Mercuria, is expected to depart around June 22, 2025. Since commencing operations, the refinery has focused on supplying the West African market. Its expansion into Asia signals growing confidence in its production capacity and a readiness to compete on a global scale. The move positions Dangote as a credible global supplier, expanding its export reach and revenue potential. For Nigeria, it signals progress toward fuel self-sufficiency, strengthens non-oil export earnings, and boosts investor confidence in the downstream sector.

Nigeria’s Inflation Eases Again in May, But Food Pressures Loom

According to the National Bureau of Statistics (NBS), Nigeria’s inflation rate eased for the second consecutive month in May 2025, with headline inflation declining by 74bps to 22.97%YoY, down from 23.71%YoY in April 2025. This decline was largely driven by a moderation in both food and core inflation, which slowed to 21.14%YoY and 22.28%YoY (vs 21.26% and 23.39% in April 2025) , respectively. The moderation was supported improved supply of key staples, stable exchange rates, and energy price relief following a cut in petrol prices. However, food inflation rose on a monthly basis to 2.19% MoM in May 2025, driven by price increases in yam, sorghum, and imported rice. Looking ahead, inflationary pressures may resurface due to seasonal planting, festive demand, and flooding in key food-producing areas. However, stable fuel prices and government interventions could help limit the impact in the near term.

CBN Halts Dividends for Banks in Breach as It Moves to Strengthen Sector Resilience

The Central Bank of Nigeria (CBN) issued a directive instructing banks with regulatory forbearance exposures or breaches of the Single Obligor Limit (SOL) to suspend dividend payments, executive bonuses, and offshore expansion plans. The move is aimed at strengthening capital buffers and addressing growing concerns that headline Capital Adequacy Ratios (CARs) may overstate resilience, particularly where large loan exposures—mainly in oil & gas and refining—remain under forbearance.

Forbearance measures, initially introduced during the pandemic, allowed banks to restructure loans without full provisioning. However, their extended use has delayed the recognition of impaired assets, masking true asset quality.

Banks such as GTCO and Stanbic IBTC, which have exited forbearance, are now better positioned to resume dividend payouts and attract yield-seeking investors. Others like Zenith Bank and FCMB are making progress toward compliance, with FCMB notably working to resolve its SOL breach through a debt-to-equity conversion.

Overall, we see the directive as a prudent clean-up measure rather than a sign of systemic risk. Well-capitalized banks with clean balance sheets remain attractive for medium- to long-term investors, especially as dividend visibility improves and regulatory clarity returns.

FG Unveils Concessionary CNG Pricing to Boost Clean, Affordable Transport Fuel

The Federal Government has introduced a new pricing framework for Compressed Natural Gas (CNG) to accelerate its adoption as a cleaner, cheaper alternative to PMS. The Concessionary Autogas Supply and Pricing Framework aims to support the transportation sector by ensuring that CNG is sold at lower rates compared to other gas categories, such as those used for power generation or industrial purposes. It also enforces full supply chain tracking to ensure transparency and market stability. Overall, the initiative aims to lower fuel costs, cut emissions, and attract more clean energy investment.

PZ Cussons Exits Palm Oil Venture in $70M Deal to Refocus on Core Business

On the corporate scene, PZ Cussons has exited Nigeria’s palm oil sector following the sale of its 50% stake in the PZ Wilmar joint venture to its long-time partner, Wilmar International, for USD70mn. The decision marks the end of a 15 years partnership and aligns with PZ Cussons’ strategy to streamline its operations, reduce debt, and focus on core categories such as personal and baby care. The exit comes amid persistent macroeconomic pressures in Nigeria, including FX volatility and rising input costs, which have weighed on the company’s bottom-line. For Wilmar, the acquisition provides full control of the business, enabling it to deepen its presence in Nigeria’s fast-growing edible oils market.

CBN NTB Auction Sees Strong Demand as Stop Rates Dip Across Tenors

At this week’s NTB Auction, the CBN offered a total of NGN162.0bn (vs NGN450.0bn at the previous auction). Total subscription was NGN1.23trn, with heavy demand on the longer tenure bill. Despite the strong interest, the CBN allotted NGN162.02bn, resulting in subscription-to-offer ratio of 7.61x . Hence, stop rates slightly decline on the 91-day, 182-day and 364-day instruments to 17.80% ,18.35% and 18.84% (vs 17.98%, 18.50% and 19.56% at the previous auction).

CBN OMO Auction Attracts Strong Demand as Rates Climb Above 24%

The CBN held an OMO auction this week to mop up excess liquidity from the system. A total of NGN600.00bn was offered in the auction. The auction saw a total subscription amount of NGN1.2trn, with NGN1.1trn ultimately allotted. Marginal rates printed at 24.20% and 24.59% at the auction.

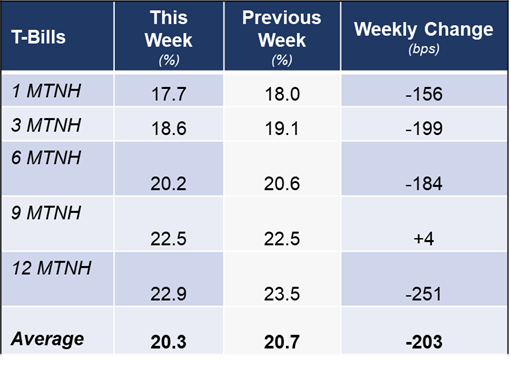

T-Bills Market Turns Bullish as Yields Drop Sharply on Renewed Demand

The fixed income market ended the week on a broadly bullish note. In the secondary T-bills market, renewed buying interest drove average yields down by 100bps to 20.5%. Demand was particularly strong for the JUN-25 (-130bps), JUN-26 (-122bps), and DEC-25 (-72bps) maturities. However, profit-taking activity weighed on the AUG-25 bill, causing its yield to rise sharply by 116bps.

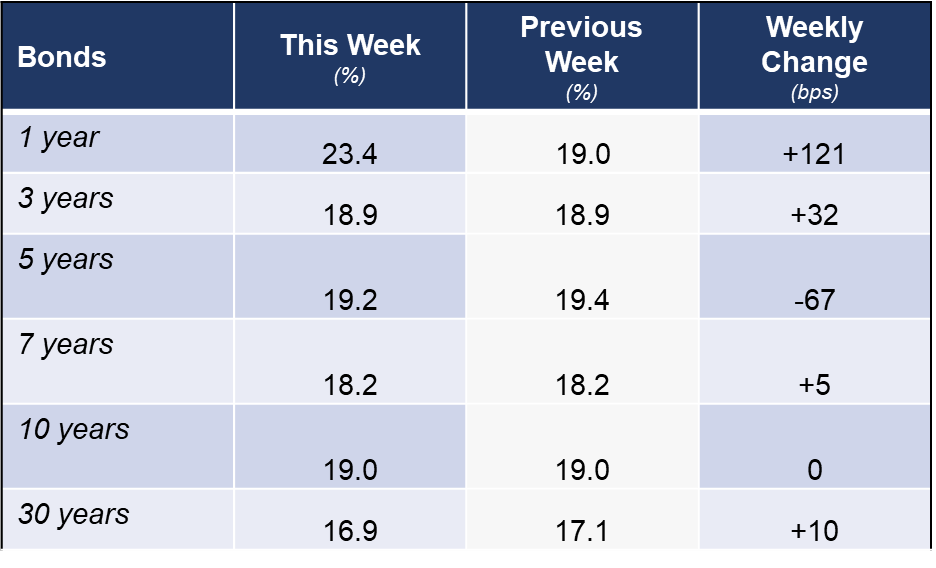

Bullish Sentiment Prevails in Bond Market as Yields Drop Across Key Tenors

Similarly, the bond market exhibited a bullish bias, as average yields declined by 27bps to 18.5%, supported by strong demand for short- and mid-tenor instruments, particularly MAR-26 (-76bps), MAR-35 (-57bps), and FEB-34 (-23bps). However, the overall rally was partially tempered by profit-taking at the short end, most notably in MAR-28, which saw yields rise by 11bps.

Eurobond Market Rallies as Yields Drop on Strong Short-End Demand

The Eurobond market also maintained a bullish tone, as average yields fell by 28bps to 8.9%, driven by the broad-based buying interest. This was especially evident at the short end, with notable yield compressions in NOV-25 (-108bps) and NOV-27 (-46bps)

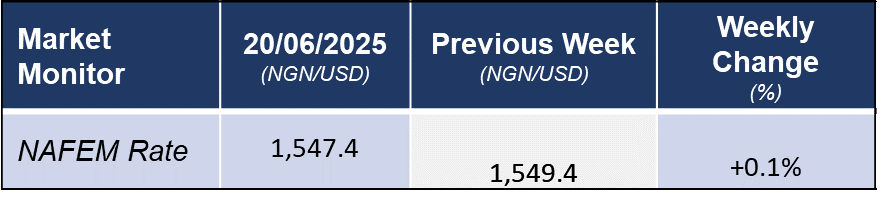

Market Snapshot

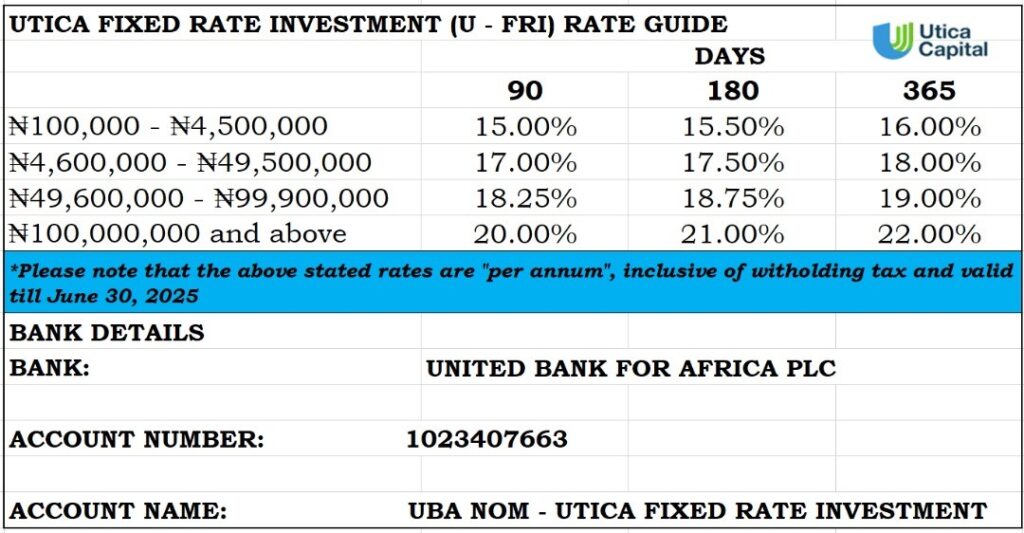

Fixed Income Opportunities for the week